- Buy Crypto

- Markets

- Futures

- Spot

- Copy Trade

Earn

Earn- More

Base contributes 70% of revenue but pays only 2.5% in rent; Superchain may be entering its "forking" countdown

Original Title: The Case for Selling $OP Before $BASE

Original Author: @13300RPM, Four Pillars Researcher

Original Translation: AididiaoJP, Foresight News

Key Points

· Highly Concentrated Revenue: By 2025, Base accounted for approximately 71% of Superchain's sequencer revenue. This concentration trend is intensifying, but Coinbase's share of payments to Optimism remains fixed at 2.5%.

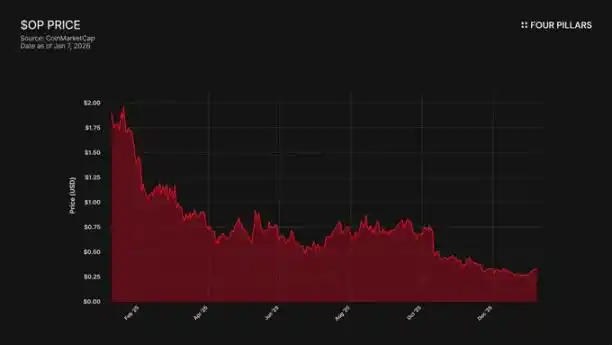

· Price-Ecosystem Divergence: The OP token has plummeted 93% from its all-time high ($4.84 → $0.32), while during the same period, Base's Total Value Locked (TVL) has increased by 48% ($31 billion → $50 billion). The market has recognized that Base's growth has not benefited OP holders, but has not yet considered the risk of Base potentially exiting.

· Technical Zero Barrier: The OP Stack adopts the MIT open-source license, meaning Coinbase can fork at any time. Currently, the only link keeping Base on Superchain is the governance relationship, and a BASE token with independent governance would sever this link entirely.

· Fragile Alliance: Optimism gifted Base 1.18 billion OP tokens to ensure long-term cooperation, but restricted its voting power to 9% of the total supply. This is not a true alignment of interests but rather a minority stake with an "exit option." If renegotiation leads to a drop in the OP price, Coinbase could cancel the revenue share obtained in exchange for this part of the grant, making it a worthwhile deal.

Base, Coinbase's L2 network, contributed approximately 71% of Superchain's sequencer revenue in 2025, yet only paid 2.5% to the Optimism Collective. The OP Stack operates under the MIT open-source license, and from a technical to a legal perspective, nothing can stop Coinbase from renegotiating terms with the threat of an exit or building independent infrastructure, rendering Superchain membership meaningless. OP holders are exposed to a single counterparty income dependency, with significant downside risks, and we believe the market has not fully recognized this.

1. Taking 71% of Revenue, Paying Only 2.5% as "Rent"

When Optimism initially inked a deal with Base, the premise was that no chain could dominate the Superchain's economic ecosystem, leading to revenue sharing imbalance. Fee splits were calculated based on the higher of "2.5% of chain revenue" or "15% of on-chain profit (revenue minus L1 Gas costs)," which seemed reasonable for a collaborative, diversified Rollup ecosystem.

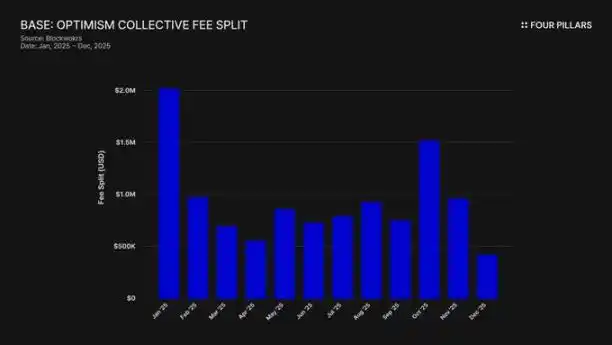

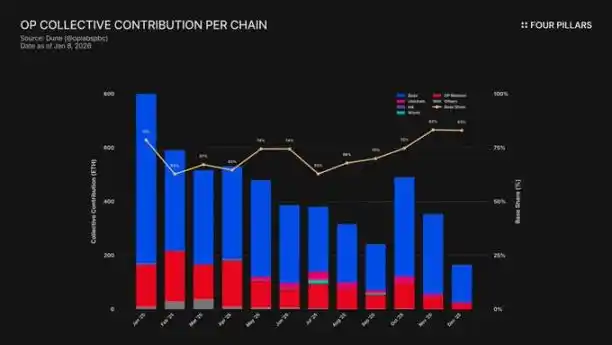

However, this assumption was wrong. By 2025, Base generated $74 million in chain revenue, accounting for over 71% of all OP chain sequencer fees, yet only paid 2.5% to the Optimism Collective. This means Coinbase received 28 times the value it put in. By October 2025, Base's TVL had reached $5 billion (a 48% growth in six months), becoming the first Ethereum L2 to cross this threshold. Since then, its dominance has only increased.

A subsidy mechanism has exacerbated this imbalance. While Base has led in revenue generation, the OP mainnet, which shares 100% of profits with the Collective, has shouldered a disproportionate contribution to the ecosystem. Essentially, the OP mainnet is subsidizing the political cohesion of this alliance, with the largest member paying the smallest share.

Where did these fees go? According to Optimism's official documentation, sequencer revenue flows into the Optimism Collective's treasury. To date, this treasury has accumulated over $34 million from Superchain fees, but these funds have not been used or allocated to any specific projects.

The envisioned "flywheel" (fee subsidizes public goods → public goods strengthen ecosystem → ecosystem generates more fees) has not yet spun up. Current projects like RetroPGF and ecosystem grants derive funds from OP token issuance, not ETH in the treasury. This is crucial as it undermines the core value proposition of joining the Superchain. Base contributes about $1.85 million annually to a treasury, yet this treasury does not provide direct economic returns to fee-paying member chains.

Governance participation also illustrates the issue. In January 2024, Base released the "Base Participation in Optimism Governance Manifesto." Since then, there has been no public action: no proposals, no forum discussions, no visible governance involvement. As the chain contributing over 70% of the economic value to Superchain, Base is notably absent from the governance process it claims to engage in. Even Optimism's own governance forums barely mention Base. The so-called "shared governance" value seems to be merely lip service to both parties.

Therefore, the "value" of Superchain membership remains entirely future-facing to this day—future interoperability, future governance influence, future network effects. For a publicly traded company accountable to shareholders, when the immediate costs are concrete and ongoing, "future value" is hard to justify.

The ultimate question boils down to: Does Coinbase have any economic incentive to maintain the status quo? And, what happens when they decide they no longer need to?

2. The Potential for an Imminent "Fork"

This is the legal reality behind all Superchain relationships: The OP Stack is a public MIT-licensed product. Anyone in the world can freely clone, fork, or deploy it without any permission.

So, what keeps chains like Base, Mode, Worldcoin, and Zora within Superchain? According to Optimism's documentation, the answer lies in a series of "soft constraints": participation in shared governance, shared upgrading and security, an ecosystem fund, and the legitimacy of the Superchain brand. Chain inclusion is voluntary, not coerced.

We believe this distinction is crucial in assessing the risk of OP.

Consider what Coinbase would lose in a fork: participation in Optimism governance, the "Superchain" brand, and a channel for coordinated protocol upgrades.

Now think about what they would retain: 100% of the $5 billion TVL, all users, all applications deployed on Base, and over $74 million in sequencer income annually.

For these "soft constraints" to hold, Base needs to obtain something from Optimism that it cannot build or buy on its own. However, there is evidence to suggest that Base is already fostering this independence. In December 2025, Base launched a cross-chain bridge directly to Solana, leveraging Coinbase's own infrastructure and built on the Chainlink CCIP instead of relying on Superchain's interoperability solution. This indicates that Base is not solely relying on Superchain's interoperability solution.

We are not claiming that Coinbase will fork tomorrow. What we want to highlight is that the MIT license itself is a fully matured "exit option," and Coinbase's recent actions suggest that they are actively reducing their dependence on the value provided by Superchain. A BASE token with its own governance scope will complete this shift, turning those "soft constraints" from meaningful restraints into purely ceremonial associations.

For OP holders, the question is simple: If the only reason to keep Base tied to Superchain is the "ecosystem alliance" facade, what happens when Coinbase decides this charade is ya not worth it anymore?

3. Negotiation, Actually Already Underway

"Exploring"—this is the standard term for every L2 in the 6-12 months leading up to the formal token launch.

In September 2025, Jesse Pollak announced at the BaseCamp conference that Base is "exploring" the issuance of a native token. He cautiously added that there is currently "no concrete plan," and Coinbase "does not intend to announce a release date anytime soon." This is noteworthy because until the end of 2024, Coinbase had made it clear that there were no plans to issue a Base token. This announcement came months after Kraken revealed its plan for the INK token on the Ink network, signaling a shift in the competitive landscape of L2 tokenization.

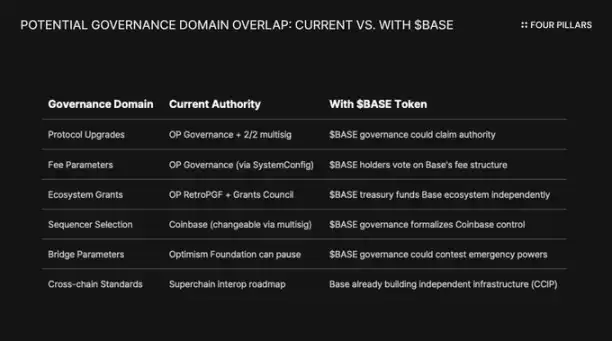

We believe that the phrasing is just as important as the substance. Pollak described the token as a "powerful lever to expand governance, ensure consistent developer incentives, and open up new design paths." None of these are neutral terms. Protocol upgrades, fee parameters, ecosystem grants, sequencer selection—these are all areas currently governed by Superchain. A BASE token with governance over these decisions will overlap with Optimism's governance, with Coinbase holding greater economic control.

To understand why the BASE token would fundamentally alter the relationship, one must first grasp the current governance mechanism of Superchain.

The Optimism Collective operates on a bicameral system:

· Token Senate (OP holders): Votes on protocol upgrades, grants, and governance proposals.

· Citizen Assembly (Badge holders): Votes on RetroPGF fund distribution.

The upgrade authority for Base is controlled by a 2/2 multisig wallet, with signatories being Base and the Optimism Foundation—neither party can unilaterally upgrade Base's contracts. Upon full implementation, the Security Council will "execute upgrades based on Optimism governance guidance."

This structure grants Optimism shared control over Base, rather than unilateral control. The 2/2 multisig is a form of checks and balances: Optimism cannot force through upgrades that Base does not want, but Base also cannot upgrade unilaterally without Optimism's signature.

If Coinbase decides to follow the path of other L2 governance tokens like ARB and OP, structural conflicts are inevitable. If BASE holders vote to upgrade the protocol, whose decision takes precedence — BASE governance or OP governance? If BASE has its own grant program, why would Base developers wait for RetroPGF? If BASE governance controls validator selection, what power is left for the 2/2 multisig?

The key point is that Optimism governance cannot prevent Base from issuing a token with a governance scope overlapping with it. The "Law of the Chain" sets out user protection and interoperability standards, but does not restrict what chain governors can do with their own tokens. Tomorrow, Coinbase could launch the BASE token with full governance rights over the Base protocol, and Optimism's only recourse would be political pressure — that increasingly toothless "soft constraint."

Another interesting angle is the constraint of a publicly traded company. This would be the first time a token generation event is led by a publicly traded company. Traditional token issuance and airdrops are designed to maximize token value for private investors and the founding team. However, Coinbase has a fiduciary duty to COIN shareholders. Any token distribution scheme must demonstrate its ability to enhance Coinbase's enterprise value.

This changes the rules of the game. Coinbase cannot simply airdrop tokens to maximize community goodwill. They need a structure that can increase COIN's stock price. One way to do this is to use the BASE token as leverage to renegotiate a lower revenue share for Superchain, thereby increasing Base's retained earnings and ultimately boosting Coinbase's financials.

4. Rebuttal on "Reputational Risk"

Perhaps the strongest counterargument to our point is that Coinbase is a publicly traded company that positions itself as a paragon of "compliance and collaboration" in the crypto space. Forking the OP Stack to save a few million dollars in revenue share each year may seem stingy and could tarnish its carefully curated brand image. This argument deserves serious consideration.

Superchain does indeed offer real value. Its roadmap includes native cross-chain communication, and the total value locked on all Ethereum L2s peaked at around $555 billion in December 2025. Base benefits from composability with the OP mainnet, Unichain, and Worldchain. Giving up these network effects comes at a cost.

Additionally, there is the 118 million OP token grant. To solidify the "long-term alliance," the Optimism Foundation granted Base the opportunity to receive approximately 118 million OP tokens over six years. At the time of the agreement, this grant was valued at around $175 million.

However, we believe this defense misapprehends the real threat. The rebuttal assumes a public, adversarial fork. A more likely path is a gentle renegotiation: Coinbase leveraging the BASE token to negotiate more favorable terms within the Superchain. This negotiation is likely to be hardly newsworthy outside of governance forums.

Consider the interoperability argument. Base has already independently built an interoperability solution separate from Optimism, establishing a bridge to Solana using CCIP. They did not wait for Superchain's interoperability solution. They are concurrently building their own cross-chain infrastructure. When you take matters into your own hands to solve the problem, the soft constraint of "shared upgrades and security" becomes less critical.

Look again at the OP grant. The power Base has to vote or delegate with these grants is capped at 9% of the votable supply. This is not a deep tie-up but a governance-light minority stake. Coinbase cannot control Optimism with 9%, but Optimism also cannot control Base with this. At the current price (around $0.32), the entire 118 million grant is valued at approximately $38 million. If post-renegotiation, the market sees a 30% drop in OP due to reduced Base revenue expectations, Coinbase's paper loss on this grant is minuscule compared to a permanent cancellation or significant cut in revenue share.

Reducing the 2.5% revenue share of over $70 million in annualized revenue to 0.5% would permanently save Coinbase over $1.4 million per year. In contrast, the one-time devaluation of the OP grant by about $10 million is merely a fraction of that.

Institutional investors are not concerned about Superchain politics. They care about Base's TVL, transaction volume, and Coinbase's profits. A revenue share renegotiation would not cause COIN stock price fluctuation. It would simply appear as a routine governance update on Optimism's forums, slightly enhancing Coinbase's L2 business profit margin.

5. A Single Income Source with an "Exit Option" Attached

We believe that OP has not yet been seen by the market as an asset with counterparty risk, but it should be.

The token has dropped 93% from its all-time high of $4.84 to around $0.32, with a circulating market cap of approximately $620 million. The market has clearly revalued OP downwards, but we believe that it has not fully digested the structural risk embedded in the Superchain economic model.

The market's divergence tells the story. Base's TVL rose from $31 billion in January 2025 to a peak of over $56 billion in October. Base is winning, but OP holders are not. Consumer attention has almost entirely shifted to Base, and despite new partners joining, OP mainnet still lags in regular user usage.

Superchain looks like a decentralized collective. But economically, it heavily relies on a single counterparty who has ample motivation to renegotiate.

Look at income concentration: Base accounts for over 71% of all Optimism Collective sequencer revenue. The reason for the high contribution ratio of the OP mainnet is not its rapid growth, but because it shares 100% of the profits, while Base only shares 2.5% or 15%.

Now, let's look at the asymmetrical income structure OP holders face:

· If Base stays and grows: OP captures 2.5% of the income. Base retains 97.5%.

· If Base renegotiates to ~0.5%: OP will lose about 80% of its income from Base. The Superchain's biggest economic contributor becomes irrelevant.

· If Base exits entirely: OP will lose its economic engine overnight.

In all three scenarios, there is limited upside potential and potentially unlimited downside. What you hold is a long position on an income stream, while the largest payer holds all the chips, including an exit option on an MIT agreement and the possibility of establishing independent governance for a new generation token at any time.

The market seems to have already digested the point that "Base's growth does not effectively benefit OP holders." But what we believe it has not yet digested is the exit risk—namely, the possibility of Coinbase leveraging the BASE token to renegotiate terms or, worse, gradually completely disengaging from Superchain governance.

You may also like

What’s Driving Crypto Markets in Early 2026: Market Swings, AI Trading, and ETF Flows?

Imagine checking Bitcoin and Ethereum prices in a day — one minute up 5%, the next down 4%. Sharp moves, quick reversals, and sensitivity to macro signals marked the first week of 2026. After an early-year rally, both assets pulled back as markets recalibrated expectations around U.S. monetary policy and institutional flows. For traders — including those relying on AI or automated systems — this period offered a vivid reminder: abundant signals do not guarantee clarity. Staying disciplined in execution is often the real challenge.

ZCash Team Split, Bank of America Upgrades Coinbase Rating, What's the Overseas Crypto Community Talking About Today?

Key Market Info Discrepancy on January 9th - A Must-Read! | Alpha Morning Report

Left Hand BTC, Right Hand AI Computing Power: The Gold and Oil of the Data Intelligence Era

Wyoming’s FRNT Stablecoin Launches — First State-Backed Stablecoin Hits Market

Key Takeaways Wyoming leads innovation in the U.S. by launching the first state-backed stablecoin, FRNT, representing a pivotal…

Why Ethereum Can’t Compete on Speed Alone

Key Takeaways Vitalik Buterin emphasizes the importance of bandwidth scaling over latency reduction for Ethereum’s future. Ethereum’s design…

Bitmine Perseveres with Ethereum Staking, Adds Over $344 Million More in ETH

Key Takeaways Bitmine has significantly increased its Ethereum holdings by adding nearly 100,000 ETH valued at $344.4 million.…

USD 1 Billion Surge in Market Cap: Behind the Scenes with Trump Family Bet and CEX Shilling

The old altcoin script is outdated, take you to decipher the new market structure

Wyoming Stablecoin FRNT Goes Live on Solana, Polycule Bot Hacked, What's the Overseas Crypto Community Talking About Today?

Visa Crypto Lead: Eight Key Evolutions of Crypto and AI by 2026

Ripple reaffirms its decision to remain private, supported by a robust balance sheet

Key Takeaways Ripple has decided against pursuing an IPO, thanks to ample internal resources and a strong balance…

Start-of-the-Year Crypto Rally Stalls: What’s Next?

Key Takeaways The initial crypto market boost at the start of 2026 has lost momentum, primarily due to…

Barclays Invests in Stablecoin Settlement Firm as Tokenized Infrastructure Expands

Key Takeaways Barclays has invested in Ubyx, a U.S.-based startup focused on developing clearing systems for tokenized forms…

Karatage Welcomes Shane O’Callaghan as Senior Partner in Strategic Move

Key Takeaways Karatage, a London-based hedge fund, appoints Shane O’Callaghan as a senior partner to enhance its institutional…

Lloyds Bank Achieves a Milestone: UK’s First Gilt Purchase via Tokenized Deposits

Key Takeaways Lloyds Bank executed the first-ever UK government gilt purchase through tokenized deposits, highlighting a transformative use…

Morgan Stanley Files for Ether Trust after Bitcoin and Solana ETF Proposals

Key Takeaways Morgan Stanley has made a significant move by filing for an Ethereum Trust with the SEC,…

2025 Crypto Bear Market: A Crucial Year for Institutional Repricing

Key Takeaways The 2025 crypto bear market witnessed significant corrections in the DeFi and smart contract sectors, setting…

What’s Driving Crypto Markets in Early 2026: Market Swings, AI Trading, and ETF Flows?

Imagine checking Bitcoin and Ethereum prices in a day — one minute up 5%, the next down 4%. Sharp moves, quick reversals, and sensitivity to macro signals marked the first week of 2026. After an early-year rally, both assets pulled back as markets recalibrated expectations around U.S. monetary policy and institutional flows. For traders — including those relying on AI or automated systems — this period offered a vivid reminder: abundant signals do not guarantee clarity. Staying disciplined in execution is often the real challenge.

ZCash Team Split, Bank of America Upgrades Coinbase Rating, What's the Overseas Crypto Community Talking About Today?

Key Market Info Discrepancy on January 9th - A Must-Read! | Alpha Morning Report

Left Hand BTC, Right Hand AI Computing Power: The Gold and Oil of the Data Intelligence Era

Wyoming’s FRNT Stablecoin Launches — First State-Backed Stablecoin Hits Market

Key Takeaways Wyoming leads innovation in the U.S. by launching the first state-backed stablecoin, FRNT, representing a pivotal…

Why Ethereum Can’t Compete on Speed Alone

Key Takeaways Vitalik Buterin emphasizes the importance of bandwidth scaling over latency reduction for Ethereum’s future. Ethereum’s design…