- Buy Crypto

- Markets

- Futures

- Spot

- Copy Trade

WE-Launch

WE-Launch

Digital banks have long ceased to make money from traditional banking services; the real goldmine lies in stablecoins and identity authentication.

Original Article Title: Neobanks Are No Longer About Banking

Original Article Author: Vaidik Mandloi, Token Dispatch

Original Article Translation: Chopper, Foresight News

Where Is the True Value Flowing for Digital Banks?

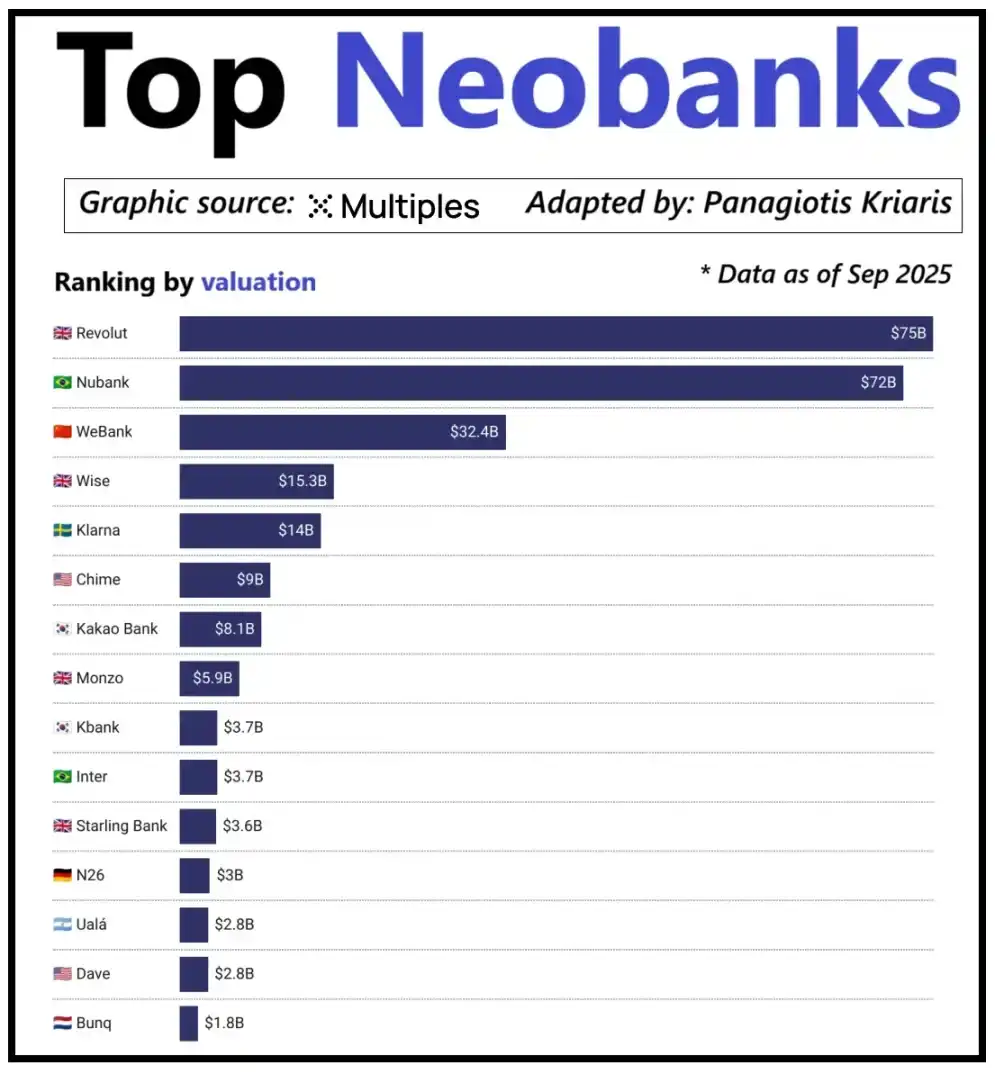

Looking at the top digital banks globally, their valuation is not simply determined by user scale but by their ability to generate revenue per user. Digital bank Revolut is a prime example: despite having fewer users than Brazilian digital bank Nubank, its valuation surpasses the latter. The reason lies in Revolut's diversified revenue streams, covering areas such as foreign exchange trading, securities trading, wealth management, and premium membership services. In contrast, Nubank's business expansion relies mainly on credit operations and interest income rather than bank card fees. China's WeBank has taken a different path of differentiation, achieving growth through extreme cost control and deep integration into the Tencent ecosystem.

Valuation of Top Emerging Digital Banks

Currently, crypto digital banks are experiencing a similar development milestone. The combination of "wallet + bank card" can no longer be called a business model, as any institution can easily launch such services. The platform's competitive advantage lies precisely in its chosen core monetization path: some platforms earn interest income from user account balances, some rely on stablecoin transaction volume for profits, and a few platforms place their growth potential in stablecoin issuance and management, as this is the most stable and predictable source of income in the market.

This also explains why the importance of the stablecoin race is becoming increasingly prominent. For reserve-backed stablecoins, their core profit comes from investment returns on reserves, i.e., the interest generated by investing reserves in short-term government bonds or cash equivalents. This income belongs to the stablecoin issuer rather than just the digital bank providing stablecoin holding and spending functions to users. This profit model is not unique to the crypto industry: in the traditional financial sector, digital banks also cannot earn interest from user deposits, and the actual custodian banks holding the funds enjoy this income. With the emergence of stablecoins, this "separation of income ownership" model has become more transparent and centralized, where entities holding short-term government bonds and cash equivalents earn interest income, while consumer-facing applications are primarily responsible for user acquisition and product experience optimization.

As the adoption of stablecoins continues to grow, a contradiction is gradually emerging: application platforms that undertake user acquisition, transaction matching, and trust building often cannot profit from the underlying reserve. This value gap is forcing enterprises to integrate into vertical domains, moving away from a mere frontend tool positioning towards the core of fund custody and management.

It is precisely due to this consideration that companies like Stripe and Circle have been increasing their efforts to lay out their strategies in the stablecoin ecosystem. They are no longer satisfied with staying at the distribution level but are expanding into the settlement and reserve management field, as this is the core profit-making area of the entire system. For example, Stripe launched its dedicated blockchain called Tempo, specifically designed for low-cost, instant transfers of stablecoins. Stripe did not rely on existing public blockchains like Ethereum or Solana but built its own transaction channels to control the settlement process, fee pricing, and transaction throughput, all of which directly translate into better economic benefits.

Circle has also adopted a similar strategy by creating a dedicated settlement network called Arc for USDC. Through Arc, inter-institution USDC transfers can be completed in real-time without causing congestion on the public chain network, nor incurring high fees. Essentially, Circle has built an independent USDC backend system through Arc, no longer being dependent on external infrastructure.

Privacy protection is another important driver of this strategy. As Prathik elaborated in the article "Reshaping the Brilliance of Blockchain," a public blockchain records every stablecoin transfer on a publicly transparent ledger. This feature is suitable for an open financial system but has drawbacks in commercial scenarios such as salary payments, supplier payments, and treasury management. In these scenarios, transaction amounts, counterparties, and payment patterns are sensitive information.

In practice, the high transparency of public chains allows third parties to easily reconstruct a company's internal financial situation through blockchain explorers and on-chain analysis tools. The Arc network enables inter-institution USDC transfers to settle outside of the public chain, preserving the advantage of fast stablecoin settlement while ensuring the confidentiality of transaction information.

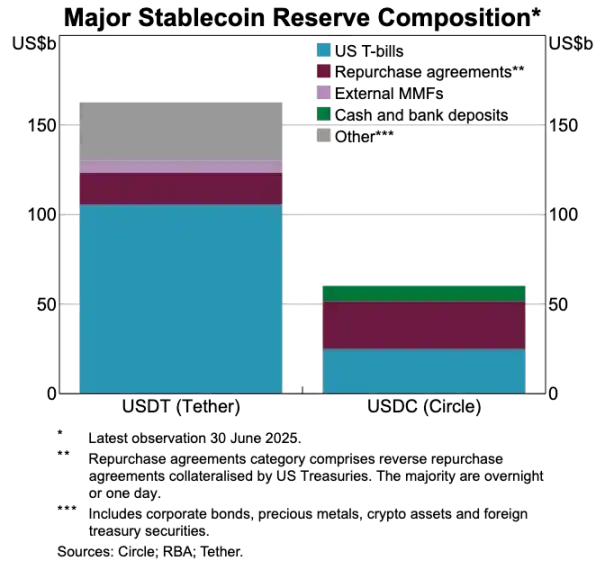

Comparison of USDT and USDC Asset Reserves

Stablecoins Are Disrupting the Old Payment System

If stablecoins are at the core of value, the traditional payment system appears increasingly outdated. The current payment process involves multiple intermediaries: the receiving gateway is responsible for fund collection, the payment processor completes transaction routing, card networks authorize transactions, and the account-holding banks of the transaction parties ultimately settle. Each step incurs costs and causes transaction delays.

Stablecoins, on the other hand, bypass this lengthy chain of intermediaries. Stablecoin transactions do not require card networks or acquirers and do not need to wait for batch settlement windows. Instead, they are based on the underlying network to facilitate direct peer-to-peer transfers. This feature has a profound impact on digital banks, as it completely changes users' experience expectations. If users can achieve instant fund transfers on other platforms, they will not tolerate the cumbersome and costly transfer processes within digital banks. Digital banks either need to deeply integrate stablecoin transaction channels or risk becoming the least efficient part of the entire payment chain.

This transformation also reshapes the business model of digital banks. In the traditional system, digital banks could earn stable fee income through bank card transactions because the payment network firmly controlled the core of transaction flow. However, in the new system dominated by stablecoins, this profit margin has been greatly compressed. Since stablecoin peer-to-peer transfers do not have transaction fees, digital banks relying solely on bank card spending for revenue are facing a completely fee-less competitive track.

Therefore, the role of digital banks is shifting from card issuers to payment routing layers. As payment methods shift from bank cards to stablecoin direct transfers, digital banks must become the core circulation nodes of stablecoin transactions. Digital banks that can efficiently process stablecoin transaction flows will dominate the market because once users see them as the default channel for fund transfers, it is challenging to switch to other platforms.

Identity Authentication is Becoming the New Generation Account Carrier

As stablecoins make payments faster and cheaper, another equally important bottleneck is gradually emerging: identity authentication. In the traditional financial system, identity authentication is a separate process: banks collect user documents, store information, and conduct verifications in the background. However, in the scenario of instant wallet fund transfers, every transaction relies on a trusted identity authentication system. Without this system, compliance checks, anti-fraud controls, and even basic permission management are not possible.

For this reason, identity authentication and payment functionality are rapidly converging. The market is gradually moving away from separate KYC processes on each platform and shifting towards a portable identity authentication system that can be used across services, countries, and platforms.

This transformation is unfolding in Europe, where the EU digital identity wallet has entered the implementation phase. The EU no longer requires each bank or application to independently conduct identity verification; instead, it has created a government-endorsed unified identity wallet that all residents and businesses can use. This wallet is used not only for identity storage but also carries various authenticated credentials (such as age, residency proof, licensing qualifications, tax information, etc.), supports users in signing electronic documents, and has built-in payment functions. Users can complete identity verification, share information on demand, and payment operations in a single process, achieving full-process seamless integration.

If the EU Digital Identity Wallet is successfully implemented, the entire European banking architecture will be restructured: Identity authentication will replace bank accounts as the core entry point for financial services. This will make identity authentication a public good, and the distinction between traditional banks and digital banks will be weakened, unless they can develop value-added services based on this trusted identity system.

The crypto industry is also evolving in the same direction. Experiments related to on-chain identity authentication have been conducted for many years. Although there is currently no perfect solution, all explorations point to the same goal: to provide users with a means of identity verification that allows them to prove their identity or relevant facts without limiting the information to a single platform.

Here are several typical examples:

· Worldcoin: Building a global-scale identity proof system that verifies users' real human identity without revealing their privacy.

· Gitcoin Passport: Integrating various credentials and verifications to reduce the risk of sybil attacks in governance voting and reward distribution processes.

· Polygon ID, zkPass, and ZK-proof frameworks: Supporting users in proving specific facts without revealing underlying data.

· Ethereum Name Service (ENS) + off-chain credentials: Allowing crypto wallets to not only display asset balances but also associate users' social identities and authentication attributes.

The goal of most crypto identity authentication projects is consistent: to enable users to autonomously prove their identity or relevant facts, and ensure that identity information is not locked into a single platform. This aligns with the EU's vision of a digital identity wallet: an identity credential that can freely flow between different applications with no need for revalidation.

This trend will also transform the operating model of digital banks. Today, digital banks see identity authentication as a core control mechanism: user registration, platform audits, ultimately forming an account subordinate to the platform. However, when identity authentication becomes a credential that users can autonomously carry, the role of digital banks shifts to being a service provider accessing this trusted identity system. This will simplify the user onboarding process, reduce compliance costs, minimize redundant verification, and allow crypto wallets to replace bank accounts as the core vessel for user assets and identity.

Future Development Trends Outlook

In conclusion, the former core elements of the digital banking system are gradually losing their competitive edge: user scale is no longer a moat, bank cards are no longer a moat, and even a streamlined user interface is no longer a moat. The real differentiation competitive barriers are reflected in three dimensions: the profit products chosen by digital banks, the fund flow channels they rely on, and the identity authentication system they access. Apart from these, other functions will gradually converge, and substitutability will become stronger.

The future successful digital banks will not be lightweight versions of traditional banks, but rather wallet-first financial systems. They will anchor on a core profit engine, which directly determines the platform's profit margin and competitive moat. Overall, the core profit engine can be divided into three categories:

Interest-Driven Digital Bank

The core competitiveness of these platforms is to become the preferred channel for users to hold stablecoins. As long as they can attract a large number of user balances, the platform can earn income through reserve-backed stablecoin interest, on-chain rewards, staking, and re-staking, without relying on a large user base. The advantage lies in the fact that the profit efficiency of asset holding is much higher than that of asset circulation. These digital banks may seem like consumer-facing applications, but they are actually modern savings platforms disguised as wallets, with the core competitiveness of providing users with a seamless interest-earning experience.

Payment Flow-Driven Digital Bank

The value proposition of these platforms comes from transaction volume. They will become the primary channel for users to send and receive stablecoin payments, and for consumption, deeply integrating payment processing, merchants, fiat-to-crypto exchanges, and cross-border payment channels. Their profit model is similar to that of global payment giants—thin profit margins per transaction, but once they become the user's preferred fund transfer channel, they can accumulate substantial income through a large transaction volume. Their moat is user habits and service reliability, becoming the default choice when users need to transfer funds.

Stablecoin Infrastructure-Driven Digital Bank

This is the deepest and potentially highest-reward track. These digital banks are not just channels for stablecoin circulation but are dedicated to controlling the issuance of stablecoins, or at least controlling their underlying infrastructure, with business scopes covering stablecoin issuance, redemption, reserve management, and settlement, among other core processes. The profit potential in this field is the most lucrative because control over the reserve directly determines income attribution. These digital banks integrate consumer-side functions with infrastructure ambitions, evolving towards a full-fledged financial network rather than just applications.

In short, Interest-Driven Digital Banks make money from user deposits, Payment Flow-Driven Digital Banks make money from user transactions, and Infrastructure-Driven Digital Banks can generate continuous profits regardless of user actions.

I anticipate that the market will diverge into two major camps: the first camp consists of consumer-facing application platforms that mainly integrate existing infrastructure, offer simple and user-friendly products, but have extremely low user conversion costs. The second camp moves towards the core area of value aggregation, focusing on stablecoin issuance, transaction routing, settlement, and identity verification integration, among other businesses.

The latter's positioning will no longer be limited to applications but as infrastructure service providers disguised in consumer-facing attire. Their user stickiness is extremely high as they quietly become the core systems for on-chain fund circulation.

You may also like

Blockchains Quietly Prepare for Quantum Threat as Bitcoin Debates Timeline

Key Takeaways: Several blockchains, including Ethereum, Solana, and Aptos, are actively preparing for the potential threat posed by…

Former SEC Counsel Explains What It Takes to Make RWAs Compliant

Key Takeaways The SEC’s shifting approach is aiding the growth of Real-World Assets (RWAs), but jurisdictional and yield…

How Ondo Finance plans to bring tokenized US stocks to Solana

Key Takeaways Ondo Finance aims to implement tokenized US stocks and ETFs on Solana by early 2026, enhancing…

Trend Research Quietly Becomes One of Ethereum’s Largest Whales with Major ETH Acquisition

Key Takeaways Trend Research has acquired 46,379 ETH, boosting their total holdings to about 580,000 ETH. The company,…

Web3 and DApps in 2026: A Utility-Driven Year for Crypto

Key Takeaways The transition to utility in the crypto sector has set a new path for 2026, emphasizing…

December 24th Market Key Intelligence, How Much Did You Miss?

Base's 2025 Report Card: Revenue Grows 30X, Solidifies L2 Leadership

The Trillion-Dollar Stablecoin Battle: Binance Decides to Step in Again

Are Those High-Raised 2021 Projects Still Alive?

Aave Community Governance Drama Escalates, What's the Overseas Crypto Community Talking About Today?

Where Did $362 Million Go? Hyperliquid Counters FUD in Decentralization Showdown

Key Market Information Discrepancy on December 24th - A Must-See! | Alpha Morning Report

Polymarket Announces In-House L2, Is Polygon's Ace Up?

Ether pumps to outsiders, dumps in-house. Can Tom Lee's team still be trusted?

Coinbase Joins Prediction Market, AAVE Governance Dispute - What's the Overseas Crypto Community Talking About Today?

Over the past 24 hours, the crypto market has shown strong momentum across multiple dimensions. The mainstream discussion has focused on Coinbase's official entry into the prediction market through the acquisition of The Clearing Company, as well as the intense controversy within the AAVE community regarding token incentives and governance rights.

In terms of ecosystem development, Solana has introduced the innovative Kora fee layer aimed at reducing user transaction costs; meanwhile, the Perp DEX competition has intensified, with the showdown between Hyperliquid and Lighter sparking widespread community discussion on the future of decentralized derivatives.

This week, Coinbase announced the acquisition of The Clearing Company, marking another significant move to deepen its presence in this field after last week's announcement of launching a prediction market on its platform.

The Clearing Company's founder, Toni Gemayel, and the team will join Coinbase to jointly drive the development of the prediction market business.

Coinbase's Product Lead, Shan Aggarwal, stated that the growth of the prediction market is still in its early stages and predicts that 2026 will be the breakout year for this field.

The community has reacted positively to this, generally believing that Coinbase's entry will bring significant traffic and compliance advantages to the prediction market. However, this has also sparked discussions about the industry's competitive landscape.

Jai Bhavnani, Founder of Rivalry, commented that for startups, if their product model proves to be successful, industry giants like Coinbase have ample reason to replicate it.

This serves as a reminder to all entrepreneurs in the crypto space that they must build significant moats to withstand competition pressure from these giants.

Regulated prediction market platform Kalshi launched its research arm, Kalshi Research, this week, aimed at opening its internal data to the academic community and researchers to facilitate exploration of prediction market-related topics.

Its inaugural research report highlights Kalshi's outperformance in predicting inflation compared to Wall Street's traditional models. Kalshi co-founder Luana Lopes Lara commented that the power of prediction markets lies in the valuable data they generate, and it is now time to better utilize this data.

Meanwhile, Kalshi announced its support for the BNB Chain (BSC), allowing users to deposit and withdraw BNB and USDT via the BSC network.

This move is seen as a significant step for Kalshi to open its platform to a broader crypto user base, aiming to unlock access to the world's largest prediction market. Furthermore, Kalshi also revealed plans to host the first Prediction Market Summit in 2026 to further drive industry engagement and development.

The AAVE community recently engaged in heated debates around an Aave Improvement Proposal (AIP) titled "AAVE Tokenomics Alignment Phase One - Ownership Governance," aiming to transfer ownership and control of the Aave brand from Aave Labs to Aave DAO.

Aave founder Stani Kulechov publicly stated his intention to vote against the proposal, believing it oversimplifies the complex legal and operational structure, potentially slowing down the development process of core products like Aave V4.

The community's reaction was polarized. Some criticized Stani for adopting a "double standard" in governance and questioned whether his team had siphoned off protocol revenue, while others supported his cautious stance, arguing that significant governance changes require more thorough discussion.

This controversy highlights the tension between the ideal of DAO governance in DeFi projects and the actual power held by core development teams.

Despite governance disputes putting pressure on the AAVE token price, on-chain data shows that Stani Kulechov himself has purchased millions of dollars' worth of AAVE in the past few hours.

Simultaneously, a whale address, 0xDDC4, which had been quiet for 6 months, once again spent 500 ETH (approximately $1.53 million) to purchase 9,629 AAVE tokens. Data indicates that this whale has accumulated nearly 40,000 AAVE over the past year but is currently in an unrealized loss position.

The founder and whale's increased holdings during market volatility were interpreted by some investors as a confidence signal in AAVE's long-term value.

In this week's top article, Morpho Labs' "Curator Explained" detailed the role of "curators" in DeFi.

The article likened curators to asset managers in traditional finance, who design, deploy, and manage on-chain vaults, providing users with a one-click diversified investment portfolio.

Unlike traditional fund managers, DeFi curators execute strategies automatically through non-custodial smart contracts, allowing users to maintain full control of their assets. The article offered a new perspective on the specialization and risk management in the DeFi space.

Another widely circulated article, "Ethereum 2025: From Experiment to Global Infrastructure," provided a comprehensive summary of Ethereum's development over the past year. The article noted that 2025 is a crucial year for Ethereum's transition from an experimental project to global financial infrastructure. Through the Pectra and Fusaka hard forks, Ethereum achieved significant reductions in account abstraction and transaction costs.

Furthermore, the SEC's clarification of Ethereum's "non-securities" nature and the launch of tokenized funds on the Ethereum mainnet by traditional financial giants like JPMorgan marked Ethereum's gaining recognition from mainstream institutions. The article suggested that whether it is the continued growth of DeFi, the thriving L2 ecosystem, or the integration with the AI field, Ethereum's vision as the "world computer" is gradually becoming a reality.

The Solana Foundation engineering team released a fee layer solution called Kora this week.

Kora is a fee relayer and signatory node designed to provide the Solana ecosystem with a more flexible transaction fee payment method. Through Kora, users will be able to achieve gas-free transactions or choose to pay network fees using any stablecoin or SPL token. This innovation is seen as an important step in lowering the barrier of entry for new users and improving Solana network's availability.

Additionally, a deep research report on propAMM (proactive market maker) sparked community interest. The report's data analysis of propAMMs on Solana like HumidiFi indicated that Solana has achieved, or even surpassed, the level of transaction execution quality in traditional finance (TradFi) markets.

For example, on the SOL-USDC trading pair, HumidiFi is able to provide a highly competitive spread for large trades (0.4-1.6 bps), which is already better than the trading slippage of some mid-cap stocks in traditional markets.

Research suggests that propAMM is making the vision of the "Internet Capital Market" a reality, with Solana emerging as the prime venue for all of this to happen.

The competition in the perpetual contract DEX (Perp DEX) space is becoming increasingly heated.

In its latest official article, Hyperliquid has positioned its emerging competitor, Lighter, alongside centralized exchanges like Binance, referring to it as a platform utilizing a centralized sequencer. Hyperliquid emphasizes its transparency advantage of being "fully on-chain, operated by a validator network, and with no hidden state."

The community widely interprets this as Hyperliquid declaring "war" on Lighter. The technical differences between the two platforms have also become a focal point of discussion: Hyperliquid focuses on ultimate on-chain transparency, while Lighter emphasizes achieving "verifiable execution" through zero-knowledge proofs to provide users with a Central Limit Order Book (CLOB)-like trading experience.

This battle over the future direction of decentralized derivatives exchanges is expected to peak in 2026.

Meanwhile, discussions about Lighter's trading fees have surfaced. Some users have pointed out that Lighter charged as much as 81 basis points (0.81%) for a $2 million USD/JPY forex trade, far exceeding the near-zero spreads of traditional forex brokers.

Some argue that Lighter does not follow a B-book model that bets against market makers, instead anchoring its prices to the TradFi market, and the high fees may be related to the current liquidity or market maker balance incentives. Providing a more competitive spread for real-world assets (RWA) in the highly volatile crypto market is a key issue Lighter will need to address in the future.

The Secret Centralization Landscape of Stablecoin Payments: 85% of Transaction Volume Controlled by Top 1000 Wallets

Why Did Market Sentiment Completely Collapse in 2025? Decoding Messari's Ten-Thousand-Word Annual Report

Audiera Sees Massive Price Surge – Key Cryptocurrency Updates

Key Takeaways Audiera (BEAT) has witnessed significant growth, experiencing a 70.10% increase in the past week. Despite the…

Blockchains Quietly Prepare for Quantum Threat as Bitcoin Debates Timeline

Key Takeaways: Several blockchains, including Ethereum, Solana, and Aptos, are actively preparing for the potential threat posed by…

Former SEC Counsel Explains What It Takes to Make RWAs Compliant

Key Takeaways The SEC’s shifting approach is aiding the growth of Real-World Assets (RWAs), but jurisdictional and yield…

How Ondo Finance plans to bring tokenized US stocks to Solana

Key Takeaways Ondo Finance aims to implement tokenized US stocks and ETFs on Solana by early 2026, enhancing…

Trend Research Quietly Becomes One of Ethereum’s Largest Whales with Major ETH Acquisition

Key Takeaways Trend Research has acquired 46,379 ETH, boosting their total holdings to about 580,000 ETH. The company,…

Web3 and DApps in 2026: A Utility-Driven Year for Crypto

Key Takeaways The transition to utility in the crypto sector has set a new path for 2026, emphasizing…

December 24th Market Key Intelligence, How Much Did You Miss?

Popular coins

Latest Crypto News

Customer Support:@weikecs

Business Cooperation:@weikecs

Quant Trading & MM:bd@weex.com

VIP Services:support@weex.com