- Buy Crypto

- Markets

- Futures

- Spot

- Copy Trade

WE-Launch

WE-Launch

Metcalfe's Law "Bankruptcy": Why Has Cryptocurrency Been Overvalued?

Original Article Title: Crypto Is Priced for Network Effects It Doesn't Have

Original Article Author: Santiago Roel Santos, Founder of Inversion

Original Article Translation: AididiaoJP, Foresight News

The Dilemma of Cryptocurrency Network Effects

My previous view on "cryptocurrency trading prices far exceeding its fundamentals" has sparked discussions. The strongest opposition is not about usage or fees but stems from ideological differences:

· "Cryptocurrency is not a business"

· "Blockchain follows Metcalfe's Law"

· "The core value lies in network effects"

As a witness to the rise of Facebook, Twitter, and Instagram, I am well aware that early internet products also faced valuation challenges. However, a pattern gradually emerged: as more users joined the social circle, the product's value experienced exponential growth. User retention strengthened, engagement deepened, and the flywheel effect became clearly visible in the experience.

This is the true manifestation of network effects.

If one advocates for "evaluating the value of cryptocurrency from a network rather than a corporate perspective," then let us delve deeper.

Upon closer examination, a glaring issue emerges: Metcalfe's Law not only fails to support the current valuation but also exposes its vulnerability.

The Misunderstood "Network Effect"

In the cryptocurrency field, the so-called "network effect" is mostly a negative effect:

· User growth leads to degraded experience

· Soaring transaction fees

· Worsening network congestion

A deeper issue lies in:

· Open-source nature causing developer attrition

· Liquidity being profit-driven

· User Cross-Chain Migration with Incentive

· Institution Platform Switch Based on Short-Term Gain

A successful network has never operated this way; the experience did not degrade when Facebook added tens of millions of users.

But the New Blockchain Has Solved the Throughput Issue

This has indeed alleviated congestion but hasn’t addressed the fundamental issue of network effects. Increasing throughput merely eliminates friction and does not create compounded value.

The fundamental contradiction still exists:

· Liquidity may drain

· Developers may migrate

· Users may depart

· Code can fork

· Weak value-capture ability

Scaling improves availability, not inevitability.

The Truth Revealed by Fees

If an L1 blockchain truly has network effects, it should capture most of the value as iOS, Android, Facebook, or Visa do. The reality is:

· L1 holds 90% of the total market value

· Fee share plummeted from 60% to 12%

· DeFi contributes 73% of fees

· But accounts for less than 10% of the valuation

The market still prices based on the "Fat Protocol Theory," but the data points to the opposite conclusion: L1 is overvalued, applications are undervalued, and the ultimate value will aggregate towards the user layer.

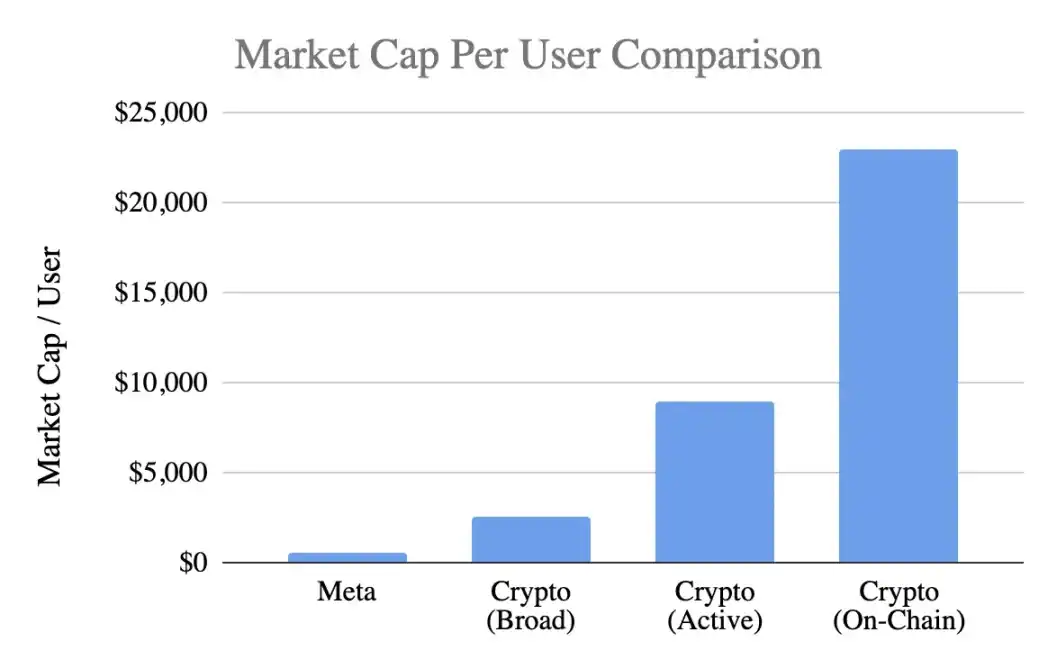

User Valuation Comparison

Using a common metric, the per-user market value:

Meta (Facebook)

· 3.1 billion monthly active users

· $1.5 trillion market cap

· Per-user value $400-500

Cryptocurrency (Excluding Bitcoin)

· $1 Trillion Market Cap

· 400 Million General Users → $2,500 per Person

· 100 Million Active Users → $9,000 per Person

· 40 Million On-chain Users → $23,000 per Person

Valuation Levels Reached:

· Optimistic Premium of 5x

· Conservative Premium of 20x

· On-chain Activity-based Premium of 50x

Meanwhile, Meta is considered the most efficient monetization engine in consumer technology.

Analysis of Development Stage

The argument of "Facebook was also like this in its early days" is worth debating. While Facebook also lacked revenue in its early days, its product had already built:

· Daily Usage Habits

· Social Connections

· Identity Verification

· Community Membership

· Value Growth from User Expansion

In contrast, the core product of cryptocurrency remains speculative, leading to:

· Rapid User Adoption

· Faster Churn

· Lack of Stickiness

· Lack of Habit Formation

· No Improvement with Scale

Unless cryptocurrency becomes "Invisible Infrastructure," a bottom-layer service imperceptible to users, network effects are challenging to self-reinforce.

This is not a maturity issue but a product essence issue.

Metcalf Law Misuse

The law's description of value≈n² is indeed appealing, but its assumptions are biased:

· Deep interaction between users (actually rare)

· Network stickiness (actually lacking)

· Value concentration (actually dispersed)

· Existence of conversion costs (actually very low)

· Building defensive moats through scale (not yet evident)

Most cryptocurrencies do not meet these prerequisites.

Insights on Key Variable k Value

In the V=k·n² model, the k value represents:

· Monetization efficiency

· Level of trust

· Depth of engagement

· Retention capability

· Conversion costs

· Ecosystem maturity

The k value for Facebook and Tencent ranges from 10⁻⁹ to 10⁻⁷, being minute due to the massive network scale.

Estimated k values for cryptocurrencies (based on a $1 trillion market cap):

· 400 million users → k≈10⁻⁶

· 100 million users → k≈10⁻⁵

· 40 million users → k≈10⁻⁴

This implies that the market assumes each crypto user's value far exceeds that of a Facebook user, despite their disadvantages in retention rate, monetization ability, and stickiness. This is not early optimism but rather overdrawn future prospects.

Current State of Real Network Effects

Cryptocurrencies actually possess:

Bilateral network effects (users ↔ developers ↔ liquidity)

Platform effects (standards, tools, composability)

These effects indeed exist but are fragile: easily forked, slow to scale, far from reaching the n² flywheel effect of Facebook, WeChat, or Visa.

Rational Perspective on Future Outlook

The vision of the “Internet being built on a cryptographic network” is indeed appealing, but it needs to be clarified:

1. This future may be realized but has not yet arrived,

2. The existing economic models have not reflected it.

The current value distribution presents:

· Cost flowing to the application layer rather than L1

· Users controlled by exchanges and wallets

· MEV capturing surplus value

· Forks weakening barriers to entry

· L1 struggling to solidify created value

Value capture is undergoing a transition from the base layer→application layer→user aggregation layer, which is favorable to users but should not warrant a premature premium.

Characteristics of a Mature Network Effect

A healthy network should exhibit:

· Stable liquidity

· Developer ecosystem concentration

· Increased base layer fee capture

· Continued retention of institutional users

· Retention rate growth across cycles

· Composability to fend off forks

Currently, Ethereum is showing initial signs, Solana is gaining momentum, with most public chains still far apart.

Conclusion: Valuation Judgment Based on Network Effect Logic

If crypto users:

· Have lower stickiness

· Monetization is more difficult

· Have higher churn rates

Then their unit value should be lower than Facebook users, not 5-50 times higher. The current valuation has overestimated the nascent network effects, and market pricing seems to imply a strong effect already exists, when in fact, it is not the case, at least not yet.

You may also like

Blockchains Quietly Prepare for Quantum Threat as Bitcoin Debates Timeline

Key Takeaways: Several blockchains, including Ethereum, Solana, and Aptos, are actively preparing for the potential threat posed by…

Three Signs that Bitcoin is Discovering its Market Bottom

Key Takeaways: Indicators suggest the selling pressure on Bitcoin is diminishing, hinting at a potential bottom. With improving…

Trump’s World Liberty Financial Token Ends 2025 Significantly Down

Key Takeaways World Liberty Financial, led by the Trump family, witnessed its token value drop by over 40%…

Former SEC Counsel Explains What It Takes to Make RWAs Compliant

Key Takeaways The SEC’s shifting approach is aiding the growth of Real-World Assets (RWAs), but jurisdictional and yield…

Kraken IPO and M&A Deals to Reignite Crypto’s ‘Mid-Stage’ Cycle

Key Takeaways: Kraken’s upcoming IPO may draw significant interest and capital from traditional finance (TradFi) investors, boosting the…

Extended Crypto ETF Outflows Indicate Institutional Pullback: Glassnode

Key Takeaways: Recent outflows from Bitcoin and Ether ETFs suggest a withdrawal of institutional interest. Institutional disengagement has…

HashKey Secures $250M for New Crypto Fund Amid Strong Institutional Interest

Key Takeaways HashKey Capital successfully secured $250 million for the initial close of its fourth crypto fund, showcasing…

Crypto Market Slump Unveils Disparity Between VC Valuations and Market Caps

Key Takeaways Recent market downturns highlight discrepancies between venture capital (VC) valuations of crypto projects and their current…

How Ondo Finance plans to bring tokenized US stocks to Solana

Key Takeaways Ondo Finance aims to implement tokenized US stocks and ETFs on Solana by early 2026, enhancing…

Philippines Cracks Down on Unlicensed Crypto Exchanges: Coinbase and Gemini Blocked

Key Takeaways The Philippine government is increasing regulatory oversight on cryptocurrency exchanges, requiring local licenses for operations. Internet…

Amplify ETFs for Stablecoins and Tokenization Begin Trading

Key Takeaways Amplify’s newly launched ETFs focus on tracking companies contributing to the development of stablecoins and tokenization…

JPMorgan Explores Cryptocurrency Trading for Institutional Clients

Key Takeaways JPMorgan Chase is considering introducing cryptocurrency trading services to its institutional clientele, marking a notable shift…

Trend Research Quietly Becomes One of Ethereum’s Largest Whales with Major ETH Acquisition

Key Takeaways Trend Research has acquired 46,379 ETH, boosting their total holdings to about 580,000 ETH. The company,…

Palmer Luckey’s Erebor Reaches $4.3B Valuation as Bank Charter Progresses

Key Takeaways: Erebor, a digital bank co-founded by Palmer Luckey, has raised $350 million, bringing its valuation to…

El Salvador’s Bitcoin Dreams Faced Reality in 2025

Key Takeaways El Salvador’s ambitious Bitcoin strategy, introduced in 2021, faced significant challenges and revisions by 2025, particularly…

Price Predictions for 12/22: SPX, DXY, BTC, ETH, BNB, XRP, SOL, DOGE, ADA, BCH

Key Takeaways: Bitcoin’s recovery efforts are met with strong resistance, indicating potential bearish trends at higher levels. Altcoins…

Trump Family-Linked USD1 Stablecoin Gains $150M as Binance Unveils Yield Program

Key Takeaways The USD1 stablecoin, associated with the Trump family, increased its market capitalization by $150 million following…

Bitcoin Perpetual Open Interest Surges as Traders Look Forward to Year-End Rally

Key Takeaways Bitcoin perpetual open interest has risen to 310,000 BTC, reflecting a bullish sentiment among traders as…

Blockchains Quietly Prepare for Quantum Threat as Bitcoin Debates Timeline

Key Takeaways: Several blockchains, including Ethereum, Solana, and Aptos, are actively preparing for the potential threat posed by…

Three Signs that Bitcoin is Discovering its Market Bottom

Key Takeaways: Indicators suggest the selling pressure on Bitcoin is diminishing, hinting at a potential bottom. With improving…

Trump’s World Liberty Financial Token Ends 2025 Significantly Down

Key Takeaways World Liberty Financial, led by the Trump family, witnessed its token value drop by over 40%…

Former SEC Counsel Explains What It Takes to Make RWAs Compliant

Key Takeaways The SEC’s shifting approach is aiding the growth of Real-World Assets (RWAs), but jurisdictional and yield…

Kraken IPO and M&A Deals to Reignite Crypto’s ‘Mid-Stage’ Cycle

Key Takeaways: Kraken’s upcoming IPO may draw significant interest and capital from traditional finance (TradFi) investors, boosting the…

Extended Crypto ETF Outflows Indicate Institutional Pullback: Glassnode

Key Takeaways: Recent outflows from Bitcoin and Ether ETFs suggest a withdrawal of institutional interest. Institutional disengagement has…

Popular coins

Latest Crypto News

Customer Support:@weikecs

Business Cooperation:@weikecs

Quant Trading & MM:bd@weex.com

VIP Services:support@weex.com