- Buy Crypto

- Markets

- Futures

- Spot

- Copy Trade

WE-Launch

WE-Launch

Messari Report Analysis: Memecoin Trading Volume Accounts for Over Half, Can Solana's Growth Myth Continue?

Original Author: MONK

Original Translation: DeepTech TechFlow

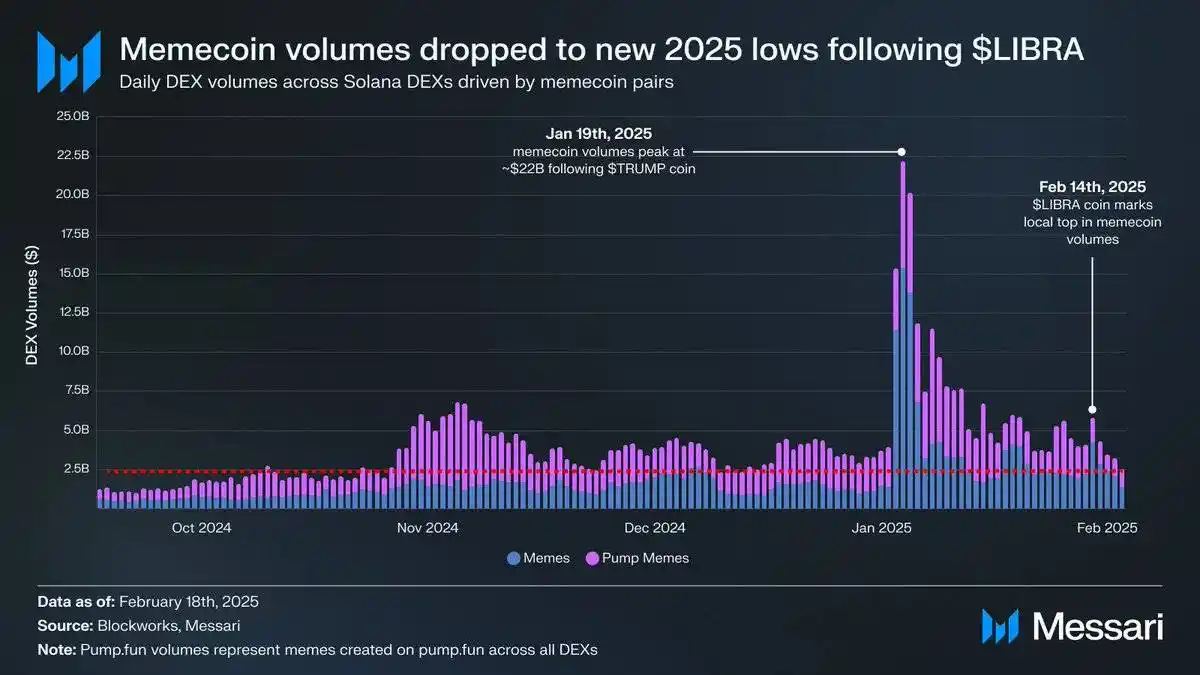

Lately, the debate over whether Memecoin is "dying" and if this will put Solana in trouble has escalated. Next, I will use data to provide you with an answer.

Since the $LIBRA event, Memecoin trading volume on Solana has dropped to the lowest level this year.

However, it is important to note that the current volume is still higher than at the beginning of 2024, indicating that Memecoin has not yet exited the stage of history.

What I really want to emphasize is the extent to which the Solana economy relies on Memecoin support.

Solana's Economic Dependence on Memecoin: Risks and Current Situation

Solana's economy is fundamentally driven by transaction volume.

If we look at the leading applications ranked by revenue on Solana, we will find that these applications are almost all protocols that in some way facilitate transaction activity.

This can be validated by the strong correlation between daily DEX trading volume and application revenue.

This pattern is not uncommon in today's high-throughput blockchains. For example, Base's economy also largely operates based on transaction volume.

In contrast, Ethereum's mainnet revenue comes more from applications driven by Total Value Locked (TVL), such as lending and mining rewards, mainly because transaction activity on the mainnet has significantly reduced.

However, it is important to note what drives this transaction volume.

On Solana, a significant amount of trading activity comes from Memecoin.

But what is concerning is that the proportion of Memecoin's trading volume has become abnormally high. For example, in February 2025, Memecoin's trading volume accounted for 70% of the total Solana DEX trading volume.

In contrast, Solana's competitor Base is gradually reducing its reliance on Memecoin trading volume and shifting towards more project tokens and trading pairs denominated in mainstream assets:

Why is this an issue?

Firstly, Solana's Memecoin volatility is extremely high, and the sustainability of these Memecoins is still in question.

More importantly, researchers, investors, and the Solana Foundation have been emphasizing the growth of application revenue and "on-chain GDP." Solana's application revenue has indeed been growing rapidly and remains one of the key metrics of user activity.

However, when we delve into the primary sources of this revenue, we find that the most profitable businesses on Solana are actually those profiting from Memecoin reliance.

For example, the two highest-earning areas on Solana are Telegram trading bots and Launchpads (such as pump.fun).

These two areas together contribute to over 60% of Solana's application revenue, with an annualized income exceeding $33 billion.

The core of these businesses is indeed Memecoin.

The interdependence in Solana's app economy further exacerbates the risk of Memecoin trading volume.

For instance, Pump relies on Raydium, Raydium relies on Jupiter, followed by Photon and Jito.

This means that a Memecoin transaction can generate revenue for five different apps simultaneously.

Therefore, these seemingly independent business apps are actually significantly interdependent in terms of revenue.

However, this cross-domain revenue is all built on the foundation of current 50%-70% of transaction volume originating from Memecoin activity.

From a blockchain perspective, Memecoin itself is not the issue. For Solana, this phenomenon is a natural outcome of its low-cost block space and early lead in on-chain user experience (UX).

The essence of blockchain should be to remain neutral to the type of activity.

Building an ecosystem around Memecoin is profitable, so many protocols have seized this opportunity.

In the future, other asset classes, such as Decentralized IoT Networks (DePIN), Real-World Assets (RWAs), stablecoins, and mainstream assets, may gradually replace Memecoin trading volume.

But for now, calling Solana a "Memecoin Economy" is not an exaggeration.

This also means that if Memecoin trading volume experiences a significant contraction, it could trigger a chain reaction of revenue decline.

Why is this important?

Solana's development narrative has always revolved around the growth of fundamental metrics, which have also supported the performance of the $SOL asset.

However, in reality, these metrics are highly dependent on the Memecoin space, which has a strong reflexivity (meaning changes in trading volume will amplify market fluctuations).

If we use these metrics to assess Solana's progress, then a collapse in Memecoin trading volume could turn a "growth story" into a "recovery story."

This would lead to a sharp shift in market sentiment, and restoring these economic activities could take a considerable amount of time.

Of course, it could also be that Murad's viewpoint is correct. If so, then disregard the above concerns.

In the long term, I still remain bullish on Solana's ecosystem. However, in the short to medium term, if Memecoin demand cannot be sustained, Solana's economy may face some challenges.

You may also like

$COIN Joins S&P 500, but Coinbase Isn't Celebrating

On May 13, S&P Dow Jones Indices announced that Coinbase would officially replace Discover Financial Services in the S&P 500 on May 19. While other companies like Block and MicroStrategy, closely tied to Bitcoin, were already part of the S&P 500, Coinbase became the first cryptocurrency exchange whose primary business is in the index. This also signifies that cryptocurrency is gradually moving from the fringes to the mainstream in the U.S.

On the day of the announcement, Coinbase's stock price surged by 23%, surpassing the $250 mark. However, just 3 days later, Coinbase was hit by two consecutive events: a hack where employees were bribed to steal customer data and a demand for a $20 million ransom, and an investigation by the U.S. Securities and Exchange Commission (SEC) into the authenticity of its claim of having over 100 million "verified users" in its securities filings and marketing materials. These two events acted as mini-bombs, and at the time of writing, Coinbase's stock had already dropped by over 7.3%.

Coincidentally, Discover Financial Services, being replaced by Coinbase, can also be considered the "Coinbase" of the previous payment era. Discover is a U.S.-based digital banking and payment services company headquartered in Illinois, founded in 1960. Its payment network, Discover Network, is the fourth largest payment network apart from Visa, Mastercard, and American Express.

In April, after the approval of the acquisition of Discover by the sixth-largest U.S. bank, Capital One, this well-established digital banking company of over 60 years smoothly handed over its S&P 500 "seat" to this emerging cryptocurrency "bank." This unexpected coincidence also portrayed the handover between the new and old eras in Coinbase's entry into the S&P 500, resembling a relay race scene. However, this relay baton also brought Coinbase's accumulated "external troubles and internal strife" to a tipping point.

Over the past decade, cryptocurrency exchanges have been the most stable "profit machines." They play a role in providing liquidity to the entire industry and rely on trading fees to sustain their operations. However, with the comprehensive rollout of ETF products in the U.S. market, this profit model is facing unprecedented challenges. As the leader in the "American stack," with over 80% of its business coming from the U.S., Coinbase is most affected by this.

Starting from the approval of Bitcoin and Ethereum spot ETFs, traditional financial capital has significantly onboarded users and funds that originally belonged to exchanges in a more cost-effective, compliant, and transparent manner. The transaction fee revenue of cryptocurrency exchanges has started to decline, and this trend may further intensify in the coming months.

According to Coinbase's 2024 Q4 financial report, the platform's total trading revenue was $417 million, a 45% year-on-year decrease. The contribution of BTC and ETH's trading revenue dropped from 65% in the same period last year to less than 50%.

This decline is not a result of a decrease in market enthusiasm. In fact, since the approval of the Bitcoin ETF in January 2024, the inflow of BTC into the U.S. market has continued to reach new highs, with asset management giants like BlackRock and Fidelity rapidly expanding their management scale. Data shows that BlackRock's iShares Bitcoin ETF (IBIT) alone has surpassed $17 billion in assets under management. As of mid-May 2025, the cumulative net inflow of 11 major institutional Bitcoin spot ETFs on the market has exceeded $41.5 billion, with a total net asset value of $1214.69 billion, accounting for approximately 5.91% of the total Bitcoin market capitalization.

Institutional investors and some retail investors are shifting towards ETF products, partly due to compliance and tax considerations. On one hand, ETFs have much lower trading costs compared to cryptocurrency exchanges. While Coinbase's spot trading fee rate varies annually in a tiered manner but averages around 1.49%, for example, the management fee for IBIT ETF is only 0.25%, and the majority of ETF institution fees fluctuate around 0.15% to 0.25%.

In other words, the more rational users are, the more likely they are to move from exchanges to ETF products, especially for investors aiming for long-term holdings.

According to multiple sources, several institutions, including VanEck and Grayscale, have submitted applications to the SEC for a Solana (SOL) ETF, with some institutions also planning to submit an XRP ETF proposal. Once approved, this may trigger a new round of fund migration. According to a report submitted by Coinbase to the SEC, as of April, the platform's trading revenue from XRP and Solana accounted for 18% and 10%, nearly one-third of the platform's fee revenue.

However, the Bitcoin and Ethereum ETFs passed in 2024 also reduced the fees for these two tokens on Coinbase from 30% and 15% to 26% and 10%, respectively. If the SOL and XRP ETFs are approved, it will further undermine the core fee revenue of exchanges like Coinbase.

The expansion of ETF products is gradually weakening the financial intermediary status of cryptocurrency exchanges. From their original roles as matchmakers and clearers to now gradually becoming mere "on-ramps and off-ramps" for funds, exchanges are seeing their marginal value squeezed by ETFs.

On May 12, 2025, SEC Chairman Paul S. Atkins gave a keynote speech at the Tokenization and Cryptocurrency Working Group roundtable. The theme of his speech revolved around "It is a new day at the SEC," where he indicated that the SEC would not approach enforcement and regulation the same way as before but would instead pave the way for cryptocurrency assets in the U.S. market.

With signs of cryptocurrency compliance such as the SEC's "NEW DAY" declaration, an increasing number of traditional brokerages are attempting to enter the cryptocurrency industry. One of the most representative cases is the well-known U.S. brokerage Robinhood, which began expanding its crypto business in 2018. By the time of its IPO in 2021, Robinhood's crypto business revenue accounted for over 50% of the company, with a significant boost from the Dogecoin "moonshot" promoted by Musk.

In Q1 2025 earnings report, Robinhood showcased strong growth, especially in revenue from cryptocurrency and options trading. Fueled by Trump's Memecoin, cryptocurrency-related revenue reached $250 million, nearly doubling year-over-year. Consequently, Robinhood Gold subscription users reached 3.5 million, a 90% increase from the previous year, with the rapid growth of Robinhood Gold providing the company with a stable source of income.

Meanwhile, RobinHood is actively pursuing acquisitions in the cryptocurrency space. In 2024, it announced a $2 billion acquisition of the long-standing European cryptocurrency exchange Bitstamp. Additionally, Canada's largest cryptocurrency CEX, WonderFi, which recently went public on the Toronto Stock Exchange, also announced its integration with RobinHood Crypto. After obtaining virtual asset licenses in the UK, Canada, Singapore, and other markets, RobinHood has taken a proactive approach in the compliant cryptocurrency trading market.

Furthermore, an increasing number of brokerage firms are exploring the same path. Futu Securities, Tiger Brokers, and others are also dipping their toes into cryptocurrency trading, with some having applied for or obtained the VA license from the Hong Kong SFC. Although their user bases are currently small, traditional brokerages have a natural advantage in user trust, regulatory licenses, and low fee structures. This could pose a threat to native cryptocurrency platforms in the future.

In April 2025, security researchers discovered that some Coinbase user data was leaked on the dark web. While the platform initially responded by attributing it to a "technical misinformation," it still raised concerns among users regarding its security and privacy protection. Just two days before Dow Jones Indexes announced Coinbase's addition to the S&P 500 Index, on May 11, 2025, Coinbase received an email from an unknown threat actor claiming to have obtained customer account information and internal documents, demanding a $20 million ransom to keep the data private. Subsequent investigations confirmed the data breach.

Cybercriminals obtained the data by bribing overseas customer service agents and support staff, mainly in "non-U.S. regions such as India." These agents abused their access to Coinbase's internal customer support system and stole customer data. As early as February this year, blockchain detective ZachXBT revealed on X platform that between December 2024 and January 2025, Coinbase users lost over $65 million to social engineering scams, with the actual amount potentially higher.

Among the victims was a well-known figure, 67-year-old Ed Suman, an established artist in the art world for nearly two decades, having been involved in the creation of artworks such as Jeff Koons' "Balloon Dog" sculpture. Earlier this year, he fell victim to an impersonation scam involving fake Coinbase customer support, resulting in a loss of over $2 million in cryptocurrency. ZachXBT critiqued Coinbase for its inadequate handling of such scams, noting that other major exchanges have not faced similar issues and recommending Coinbase to enhance its security measures.

Amidst a series of ongoing social engineering incidents, although there has not been any impact on user assets at the technical level so far, it has raised concerns among many retail and institutional investors. Especially institutions holding massive assets on Coinbase. Just considering the U.S. BTC ETF institutions, as of mid-May 2025, they collectively hold nearly 840,000 BTC, and 75% of these are custodied by Coinbase. If we price BTC at $100,000, this amount reaches a staggering $63 billion, which is equivalent to the nominal GDP of two Iceland in the year 2024.

In addition, Coinbase Custody also serves over 300 institutional clients, including hedge funds, family offices, pension funds, and endowments. As of the Q1 2025 financial report, Coinbase's total assets under management (including institutional and retail clients) reached $404 billion. The specific amount of institutional custodied assets was not explicitly disclosed in the latest report, but it should still be over 50% based on the Q4 2024 report.

Once this security barrier is breached, not only could the rate of user attrition far exceed expectations, but more importantly, institutional trust in it would undermine the foundation of its business. Therefore, after a hacking event, Coinbase's stock price plummeted significantly.

Facing a decline in spot trading fee revenue, Coinbase is also accelerating its transformation, attempting to find growth opportunities in derivatives and emerging assets. Coinbase acquired a stake in the options platform Deribit at the end of 2024 and announced the official launch of perpetual contract products in 2025. This acquisition fills in Coinbase's gap in options trading and its relatively small global market share.

Deribit has a strong presence in non-U.S. markets, especially in Asia and Europe. The acquisition has enabled Coinbase to gain a dominant position in bitcoin and ethereum options trading on Deribit, accounting for approximately 80% of the global options trading volume, with daily trading volume remaining above $2 billion.

Meanwhile, 80-90% of Deribit's customer base consists of institutional investors, with their professionalism and liquidity in the Bitcoin and Ethereum options market highly favored by institutions. Coinbase's compliance advantage, coupled with its already robust institutional ecosystem, makes it even more suitable. By using institutions as an entry point, it can face the squeeze from giants like Binance and OKX in the derivatives market.

Facing a similar dilemma is Kraken, which is attempting to replicate Binance Futures' model in non-U.S. markets. Since the derivatives market relies more on professional users, fee rates are relatively higher and stickiness is stronger, making it a significant source of revenue for exchanges. In the first half of 2025, Kraken completed the acquisition of TradeStation Crypto and a futures exchange, aiming to build a complete derivatives trading ecosystem to hedge the risk of declining spot transaction fee income.

With the surge of Memecoin in 2024, Binance, OKX, and various CEX platforms began massively listing small-market-cap, highly volatile tokens to activate active trading users. Due to the wealth effect and trading activity of Memecoins, Coinbase was also forced to join the battle, successively listing popular tokens from the Solana ecosystem such as BOOK OF MEME and Dogwifhat. Although these coins are controversial, they are frequently traded, with fee rates several times higher than mainstream coins, serving as a "blood-boosting" method for spot trading.

However, due to its status as a publicly traded company, this practice is a riskier endeavor for Coinbase. Even in the current crypto-friendly environment, the SEC is still investigating whether tokens like SOL, ADA, and SAND constitute securities.

In addition to the forced transformation strategies carried out by the aforementioned CEXs, they are also starting to lay out RWAs and the most talked-about stablecoin payment fields, such as the PYUSD launched through a collaboration between Coinbase and Paypal, Coinbase's support for the Euro stablecoin EURC by Circle that complies with EU MiCA regulatory requirements, or the USD1 launched through a collaboration between Binance and WIFL. In the increasingly crowded trading field, many CEXs have shifted their focus from just the trading market to the application field.

The golden age of transaction fees has quietly ended, and the second half of the crypto exchange platform game has silently begun.

Arthur Hayes: Why I'm Betting on ETH While the Market Is Obsessed with SOL

Deconstructing Binance Alpha2.0's New "Asia-Led Liquidity Mining" Model

How to Get Rich in Crypto Without Relying on Luck? Financial Veteran Raoul Pal's Macro Insights and Investment Path

Key Market Insight Discrepancy on May 2nd - A Must-Read! | Alpha Morning Report

Gate.io MemeBox has officially integrated with the Solana ecosystem, providing lightning-fast on-chain asset trading.

Taking Stock of the Top 10 Emerging Launchpad Platforms: Who Will Succeed in Disrupting Pump.fun?

GoRich Officially Launched: On-Chain Transactions with Zero Barrier to Entry, Even Beginners Can Catch 100x Meme Coins

Parse Haedal Protocol: Sui Liquidity Staking Gem Project, TVL Ratio Exceeds Sum of Competitors

LetsBONK's market cap surpasses $30 million in just 6 hours, Raydium launches counterattack against Pumpfun

This Week in Review | Trump to Host Dinner for TRUMP Holders; Musk and US Treasury Secretary Engage in Heated Argument at the White House

Key Market Information Discrepancy on April 27th - A Must-Read! | Alpha Morning Report

Cryptocurrency Market Sentiment Warms Up, MCP Emerges as New AI Frontier

Solana Validator Shake-Up: Foundation Aims for Decentralization, Half Validators Face Survival Test

Emotions are down, data is holding strong: Can the Memecoin make a comeback?

History Doesn’t Repeat, But It Rhymes — Don’t Miss It This Time

Key Market Information Gap on April 25th - A Must-See! | Alpha Morning Report

From BTC to SOL: A New Direction for Traditional Corporate Crypto Asset Allocation

$COIN Joins S&P 500, but Coinbase Isn't Celebrating

On May 13, S&P Dow Jones Indices announced that Coinbase would officially replace Discover Financial Services in the S&P 500 on May 19. While other companies like Block and MicroStrategy, closely tied to Bitcoin, were already part of the S&P 500, Coinbase became the first cryptocurrency exchange whose primary business is in the index. This also signifies that cryptocurrency is gradually moving from the fringes to the mainstream in the U.S.

On the day of the announcement, Coinbase's stock price surged by 23%, surpassing the $250 mark. However, just 3 days later, Coinbase was hit by two consecutive events: a hack where employees were bribed to steal customer data and a demand for a $20 million ransom, and an investigation by the U.S. Securities and Exchange Commission (SEC) into the authenticity of its claim of having over 100 million "verified users" in its securities filings and marketing materials. These two events acted as mini-bombs, and at the time of writing, Coinbase's stock had already dropped by over 7.3%.

Coincidentally, Discover Financial Services, being replaced by Coinbase, can also be considered the "Coinbase" of the previous payment era. Discover is a U.S.-based digital banking and payment services company headquartered in Illinois, founded in 1960. Its payment network, Discover Network, is the fourth largest payment network apart from Visa, Mastercard, and American Express.

In April, after the approval of the acquisition of Discover by the sixth-largest U.S. bank, Capital One, this well-established digital banking company of over 60 years smoothly handed over its S&P 500 "seat" to this emerging cryptocurrency "bank." This unexpected coincidence also portrayed the handover between the new and old eras in Coinbase's entry into the S&P 500, resembling a relay race scene. However, this relay baton also brought Coinbase's accumulated "external troubles and internal strife" to a tipping point.

Over the past decade, cryptocurrency exchanges have been the most stable "profit machines." They play a role in providing liquidity to the entire industry and rely on trading fees to sustain their operations. However, with the comprehensive rollout of ETF products in the U.S. market, this profit model is facing unprecedented challenges. As the leader in the "American stack," with over 80% of its business coming from the U.S., Coinbase is most affected by this.

Starting from the approval of Bitcoin and Ethereum spot ETFs, traditional financial capital has significantly onboarded users and funds that originally belonged to exchanges in a more cost-effective, compliant, and transparent manner. The transaction fee revenue of cryptocurrency exchanges has started to decline, and this trend may further intensify in the coming months.

According to Coinbase's 2024 Q4 financial report, the platform's total trading revenue was $417 million, a 45% year-on-year decrease. The contribution of BTC and ETH's trading revenue dropped from 65% in the same period last year to less than 50%.

This decline is not a result of a decrease in market enthusiasm. In fact, since the approval of the Bitcoin ETF in January 2024, the inflow of BTC into the U.S. market has continued to reach new highs, with asset management giants like BlackRock and Fidelity rapidly expanding their management scale. Data shows that BlackRock's iShares Bitcoin ETF (IBIT) alone has surpassed $17 billion in assets under management. As of mid-May 2025, the cumulative net inflow of 11 major institutional Bitcoin spot ETFs on the market has exceeded $41.5 billion, with a total net asset value of $1214.69 billion, accounting for approximately 5.91% of the total Bitcoin market capitalization.

Institutional investors and some retail investors are shifting towards ETF products, partly due to compliance and tax considerations. On one hand, ETFs have much lower trading costs compared to cryptocurrency exchanges. While Coinbase's spot trading fee rate varies annually in a tiered manner but averages around 1.49%, for example, the management fee for IBIT ETF is only 0.25%, and the majority of ETF institution fees fluctuate around 0.15% to 0.25%.

In other words, the more rational users are, the more likely they are to move from exchanges to ETF products, especially for investors aiming for long-term holdings.

According to multiple sources, several institutions, including VanEck and Grayscale, have submitted applications to the SEC for a Solana (SOL) ETF, with some institutions also planning to submit an XRP ETF proposal. Once approved, this may trigger a new round of fund migration. According to a report submitted by Coinbase to the SEC, as of April, the platform's trading revenue from XRP and Solana accounted for 18% and 10%, nearly one-third of the platform's fee revenue.

However, the Bitcoin and Ethereum ETFs passed in 2024 also reduced the fees for these two tokens on Coinbase from 30% and 15% to 26% and 10%, respectively. If the SOL and XRP ETFs are approved, it will further undermine the core fee revenue of exchanges like Coinbase.

The expansion of ETF products is gradually weakening the financial intermediary status of cryptocurrency exchanges. From their original roles as matchmakers and clearers to now gradually becoming mere "on-ramps and off-ramps" for funds, exchanges are seeing their marginal value squeezed by ETFs.

On May 12, 2025, SEC Chairman Paul S. Atkins gave a keynote speech at the Tokenization and Cryptocurrency Working Group roundtable. The theme of his speech revolved around "It is a new day at the SEC," where he indicated that the SEC would not approach enforcement and regulation the same way as before but would instead pave the way for cryptocurrency assets in the U.S. market.

With signs of cryptocurrency compliance such as the SEC's "NEW DAY" declaration, an increasing number of traditional brokerages are attempting to enter the cryptocurrency industry. One of the most representative cases is the well-known U.S. brokerage Robinhood, which began expanding its crypto business in 2018. By the time of its IPO in 2021, Robinhood's crypto business revenue accounted for over 50% of the company, with a significant boost from the Dogecoin "moonshot" promoted by Musk.

In Q1 2025 earnings report, Robinhood showcased strong growth, especially in revenue from cryptocurrency and options trading. Fueled by Trump's Memecoin, cryptocurrency-related revenue reached $250 million, nearly doubling year-over-year. Consequently, Robinhood Gold subscription users reached 3.5 million, a 90% increase from the previous year, with the rapid growth of Robinhood Gold providing the company with a stable source of income.

Meanwhile, RobinHood is actively pursuing acquisitions in the cryptocurrency space. In 2024, it announced a $2 billion acquisition of the long-standing European cryptocurrency exchange Bitstamp. Additionally, Canada's largest cryptocurrency CEX, WonderFi, which recently went public on the Toronto Stock Exchange, also announced its integration with RobinHood Crypto. After obtaining virtual asset licenses in the UK, Canada, Singapore, and other markets, RobinHood has taken a proactive approach in the compliant cryptocurrency trading market.

Furthermore, an increasing number of brokerage firms are exploring the same path. Futu Securities, Tiger Brokers, and others are also dipping their toes into cryptocurrency trading, with some having applied for or obtained the VA license from the Hong Kong SFC. Although their user bases are currently small, traditional brokerages have a natural advantage in user trust, regulatory licenses, and low fee structures. This could pose a threat to native cryptocurrency platforms in the future.

In April 2025, security researchers discovered that some Coinbase user data was leaked on the dark web. While the platform initially responded by attributing it to a "technical misinformation," it still raised concerns among users regarding its security and privacy protection. Just two days before Dow Jones Indexes announced Coinbase's addition to the S&P 500 Index, on May 11, 2025, Coinbase received an email from an unknown threat actor claiming to have obtained customer account information and internal documents, demanding a $20 million ransom to keep the data private. Subsequent investigations confirmed the data breach.

Cybercriminals obtained the data by bribing overseas customer service agents and support staff, mainly in "non-U.S. regions such as India." These agents abused their access to Coinbase's internal customer support system and stole customer data. As early as February this year, blockchain detective ZachXBT revealed on X platform that between December 2024 and January 2025, Coinbase users lost over $65 million to social engineering scams, with the actual amount potentially higher.

Among the victims was a well-known figure, 67-year-old Ed Suman, an established artist in the art world for nearly two decades, having been involved in the creation of artworks such as Jeff Koons' "Balloon Dog" sculpture. Earlier this year, he fell victim to an impersonation scam involving fake Coinbase customer support, resulting in a loss of over $2 million in cryptocurrency. ZachXBT critiqued Coinbase for its inadequate handling of such scams, noting that other major exchanges have not faced similar issues and recommending Coinbase to enhance its security measures.

Amidst a series of ongoing social engineering incidents, although there has not been any impact on user assets at the technical level so far, it has raised concerns among many retail and institutional investors. Especially institutions holding massive assets on Coinbase. Just considering the U.S. BTC ETF institutions, as of mid-May 2025, they collectively hold nearly 840,000 BTC, and 75% of these are custodied by Coinbase. If we price BTC at $100,000, this amount reaches a staggering $63 billion, which is equivalent to the nominal GDP of two Iceland in the year 2024.

In addition, Coinbase Custody also serves over 300 institutional clients, including hedge funds, family offices, pension funds, and endowments. As of the Q1 2025 financial report, Coinbase's total assets under management (including institutional and retail clients) reached $404 billion. The specific amount of institutional custodied assets was not explicitly disclosed in the latest report, but it should still be over 50% based on the Q4 2024 report.

Once this security barrier is breached, not only could the rate of user attrition far exceed expectations, but more importantly, institutional trust in it would undermine the foundation of its business. Therefore, after a hacking event, Coinbase's stock price plummeted significantly.

Facing a decline in spot trading fee revenue, Coinbase is also accelerating its transformation, attempting to find growth opportunities in derivatives and emerging assets. Coinbase acquired a stake in the options platform Deribit at the end of 2024 and announced the official launch of perpetual contract products in 2025. This acquisition fills in Coinbase's gap in options trading and its relatively small global market share.

Deribit has a strong presence in non-U.S. markets, especially in Asia and Europe. The acquisition has enabled Coinbase to gain a dominant position in bitcoin and ethereum options trading on Deribit, accounting for approximately 80% of the global options trading volume, with daily trading volume remaining above $2 billion.

Meanwhile, 80-90% of Deribit's customer base consists of institutional investors, with their professionalism and liquidity in the Bitcoin and Ethereum options market highly favored by institutions. Coinbase's compliance advantage, coupled with its already robust institutional ecosystem, makes it even more suitable. By using institutions as an entry point, it can face the squeeze from giants like Binance and OKX in the derivatives market.

Facing a similar dilemma is Kraken, which is attempting to replicate Binance Futures' model in non-U.S. markets. Since the derivatives market relies more on professional users, fee rates are relatively higher and stickiness is stronger, making it a significant source of revenue for exchanges. In the first half of 2025, Kraken completed the acquisition of TradeStation Crypto and a futures exchange, aiming to build a complete derivatives trading ecosystem to hedge the risk of declining spot transaction fee income.

With the surge of Memecoin in 2024, Binance, OKX, and various CEX platforms began massively listing small-market-cap, highly volatile tokens to activate active trading users. Due to the wealth effect and trading activity of Memecoins, Coinbase was also forced to join the battle, successively listing popular tokens from the Solana ecosystem such as BOOK OF MEME and Dogwifhat. Although these coins are controversial, they are frequently traded, with fee rates several times higher than mainstream coins, serving as a "blood-boosting" method for spot trading.

However, due to its status as a publicly traded company, this practice is a riskier endeavor for Coinbase. Even in the current crypto-friendly environment, the SEC is still investigating whether tokens like SOL, ADA, and SAND constitute securities.

In addition to the forced transformation strategies carried out by the aforementioned CEXs, they are also starting to lay out RWAs and the most talked-about stablecoin payment fields, such as the PYUSD launched through a collaboration between Coinbase and Paypal, Coinbase's support for the Euro stablecoin EURC by Circle that complies with EU MiCA regulatory requirements, or the USD1 launched through a collaboration between Binance and WIFL. In the increasingly crowded trading field, many CEXs have shifted their focus from just the trading market to the application field.

The golden age of transaction fees has quietly ended, and the second half of the crypto exchange platform game has silently begun.

Arthur Hayes: Why I'm Betting on ETH While the Market Is Obsessed with SOL

Deconstructing Binance Alpha2.0's New "Asia-Led Liquidity Mining" Model

How to Get Rich in Crypto Without Relying on Luck? Financial Veteran Raoul Pal's Macro Insights and Investment Path

Key Market Insight Discrepancy on May 2nd - A Must-Read! | Alpha Morning Report

Gate.io MemeBox has officially integrated with the Solana ecosystem, providing lightning-fast on-chain asset trading.

Popular coins

Latest Crypto News

Customer Support:@weikecs

Business Cooperation:@weikecs

Quant Trading & MM:bd@weex.com

VIP Services:support@weex.com