- Buy Crypto

- Markets

- Futures

- Spot

- Copy Trade

WE-Launch

WE-Launch

Each to Their Own, Every Public Blockchain Has Its Purpose

Original Title: "The Public Chain Fate Has Secretly Marked Its Purpose for You"

Original Source: Deep Tide TechFlow

The future of the industry, the future of public chains, remains undecided.

Looking back on the last market cycle, the biggest play can actually be summarized as PVP. Go PVP here, go PVP there, go PVP on any chain that still has some heat and narrative.

As we enter 2025, these chains have also entered the stage of stock competition --- from the hundred-chain war for the title of Ethereum killer a few years ago, to now most chains being labeled as "not even good enough for dogs," the remaining ones are also striving to solve their own survival problems.

Not only are the junior players PVPing, these chains are also PVPing. It's just that each chain seems to want to replicate Solana's excitement, but no matter how they toss and turn, they cannot replicate Solana's Meme frenzy.

One place nurtures one person, and perhaps one public chain can only do one thing. Every surviving public chain has already had its purpose secretly marked.

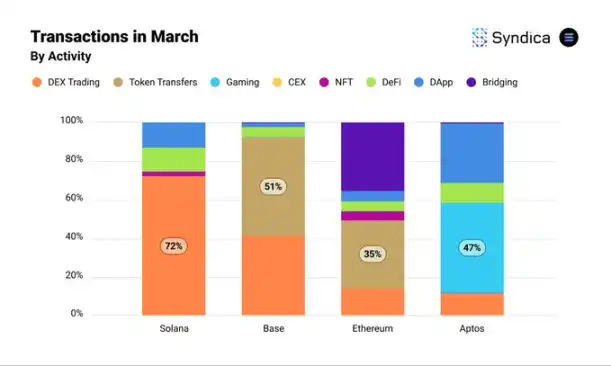

Recently, an overseas news and research institution Syndica (@Syndica_io) released a March L1/L2 Data Insight Report, making this sense of fate more tangible through numbers:

· In all Solana transactions, 72% are related to decentralized exchanges (DEXes), obviously in line with your impression of "fighting dogs."

· Base has 51% of transactions used for token transfers;

· ETH has nearly 40% of transactions used for cross-chain transfers (shown as the purple bars in the above image)

Delphi Digital's Research Lead @ceterispar1bus, when faced with this set of data, directly pointed out the essence:

Solana is for transactions, Base is for Coinbase's USDC accounting, Ethereum is for cross-chain asset transfers

As the industry has come to this point today, projects are no longer simply competing technically, but finding their own "anchor" --- a purpose positioning that makes perfect sense.

It's an Identity Tag, But More Importantly, It's Fate

On the surface, the use case of a public blockchain seems to be chosen by users and the market. However, upon deeper reflection, it appears more like the result of the covert pricing of resources and background.

Summarizing the identity tags of three public blockchains:

Solana is a transaction hotbed, Base has become Coinbase's "chief accountant," and Ethereum has been hijacked by bridges, accelerating asset outflows. Behind the current state of each chain, there are both technical and non-technical driving forces.

Let's start with Solana.

In 2025, Solana's on-chain ecosystem remains the liveliest meme transaction hotbed in the industry. The DEX trading volume in its ecosystem has securely held the top spot for two consecutive months, with a commanding market share lead. Since October 2024, Solana has been minting over 500,000 MEME coins every month, resembling an endless "meme dog party."

The junior devs are enthusiastic about sitting idle and finding angles, traders are busy monitoring pools and front-running, and those who have played with memes mention Solana, with their first reaction being, "Isn't this chain just a big casino?"

Solana's high throughput (TPS is 12 times that of Base) and low cost (a high percentage of transactions below $0.01) form the foundation of its transaction hotbed. According to the Syndicate report, Solana leads in small trades (under $100), making it suitable for high-frequency meme coin trading.

When it comes to decentralization, the practical and sensory aspects may not be that important. More crucial is the startup advantage based on resource endowment.

From 2019 to 2023, Solana received investment support from a16z, Multicoin Capital, and others, attracting DeFi and meme coin developers through grants and incubators. Solana's Breakpoint conference also often serves as an inspiration for meme coins. Do you remember two years ago when Toly wore a green cartoon dragon costume at the conference, igniting subsequent attention to the phenomenon-level meme SillyDragon?

Founders actively shape their image, intentionally or unintentionally implying a certain meme connection, which has gradually become a common practice today. Community culture has also "reserved" its meme soil, turning Solana into a "grassroots player" paradise. Through social media (such as X) and meme coin competitions, Solana has become a playground for "grassroots players," and successes like PEPE, BONK, and POPCAT have formed positive feedback loops.

User mindset is boxed in: "Solana=Transactions," and all kinds of shady Devs have flocked in, making Pumpfun's appearance seem natural.

Let's talk about Base.

There are also Memes on Base, and in the recent wave of AI Agent hype, there is no lack of standout tokens in the ecosystem. However, this seems more like a result of previous Solana fund overflow and low PvP difficulty arbitrage behavior. Data from March shows that 51% of transactions on Base are token transfers, with a deeper reason being the relationship between Coinbase and Circle.

In 2018, Coinbase and Circle jointly established the Centre Consortium, an organization specifically responsible for issuing and managing USDC. As joint initiators, Coinbase and Circle not only promoted the widespread adoption of USDC but also established operational standards for USDC through Centre. Base, as Coinbase's "brainchild," became the preferred channel for USDC transfers.

Furthermore, recent IPO filings from Circle indicate that Coinbase and Circle have a clear revenue-sharing agreement on USDC—Coinbase takes 50% of the residual income from USDC reserves. This means that every time Coinbase settles a USDC transaction or promotes the use of USDC, they get a piece of the pie.

Base's low cost and high efficiency are ideal for this "bookkeeping" need—whether it's internal fund transfers at Coinbase or user USDC transactions, Base can efficiently record and manage these on-chain activities, such as transaction records, liquidity management, and settlement operations. This "bookkeeping" not only reduces Coinbase's operating costs but also generates direct revenue through USDC income sharing.

Looking at the ecosystem culture, Base is more inclined to serve institutions and compliant users. Coinbase's 100+ million users are mostly "legitimate players," so developers naturally wouldn't choose Base to hold wild "meme parties." Base was strategically designated as the "accountant" of USDC by Coinbase and Circle from its inception, firmly locked within this duo's interest chain.

Speaking of Ethereum, it is undoubtedly a disappointing old topic. Nearly 40% of the transactions are related to cross-chain bridging, turning Ethereum into a "transit station" for other blockchains.

The price of ETH seems more like being roasted over the fire, gradually losing its moisture. Although Ethereum is still the leader in DeFi, with a TVL dominance of over 60% (Syndica data), the community's negative sentiment is spreading. Ethereum's "bridging destiny" is technically driven by high Gas fees. When the market is bullish, regular users are already overwhelmed, and they can only transfer assets to a lower-cost chain through cross-chain bridges; not to mention when the market is bearish and there is nothing to do.

Furthermore, ETH's mainnet throughput is limited, far behind Solana's high performance, and the low transaction efficiency further increases the demand for cross-chain transactions. A deeper-rooted reason comes from the diversion of historical status.

As the earliest smart contract platform, Ethereum has accumulated the most assets and dApps, naturally becoming a hub for cross-chain bridging. The ecological path dependence has led DeFi projects and funds to concentrate on Ethereum, but the high costs force users to go out, making bridging a "necessary choice." At the same time, the rise of Layer 2 has diverted users, multiple rounds of adjustments by the Ethereum Foundation, accusations of Vitalik not focusing on the main task alongside women, and the plummeting coin price where even breathing seems to be wrong...

The dream is the "world computer," but the reality is the "ATM." Its destiny seems to be locked by network effects and market changes, transforming from the DeFi overlord into an asset transfer station. Ethereum's breakout path is likely to be more challenging than Solana and Base.

Accept Destiny, Find Anchors

In the public chain competition of 2025, it is no longer the frenzy of a hundred-chain war but a calm game of existing resources. The survival path of the public chain ultimately lies in "accepting destiny, finding anchors." Transactions can be anchors, the circulation of stablecoins can be anchors, and even cross-chain can be anchors. However, the solidification of "anchors" also means that the imaginative space of the public chain is compressed.

Can Solana shake off the label of the "Meme Casino"? Can Base break free from the "bookkeeper" framework? Can Ethereum break out of the "transit station"? These questions do not have definitive answers. But ironically, most P players are not concerned about these issues.

They simply go to whichever chain is trending to "fight," or they go to whichever chain has arbitrage opportunities to "earn." The battle of public chains is actually just the background behind every passerby eager to cash in and fantasize about a thousandfold return. Perhaps only the arrival of the next cycle can provide a true answer—who can attract incremental gains, who can find new "anchors."

The future of the industry, the future of public blockchains, still hangs in the balance.

You may also like

a16z Leads $18M Seed Round for Catena Labs, Crypto Industry Bets on Stablecoin AI Payment

Never Underestimate the Significance of the US Stablecoin 'Infrastructure Bill'

If the US stablecoin bill, the "GENIUS Act," passes smoothly this time, its significance will be tremendous. I even think it's significant enough to enter the top five in Crypto history.

Although abbreviated as the GENIUS Act, which translates directly to the Genius Act, it is actually the Guiding and Establishing National Innovation for U.S. Stablecoins, which translates to "Guiding and Establishing National Innovation for US Dollar Stablecoins."

The proposal is lengthy, with several key points summarized for everyone:

· Mandatory 1:1 Full Asset Backing: Assets include cash, demand deposits, and short-term US Treasuries. At the same time, misappropriation and rehypothecation are strictly prohibited.

· High-Frequency Disclosure: Reserve reports must be published at least monthly, introducing external audits.

· Licensing Requirement: Once the circulating market cap of the issuer's stablecoin exceeds $100 billion, it must transition into the federal regulatory system within a specified timeframe, adopting banking-grade regulation.

· Introduction of Custody: The custodian of the stablecoin and its reserve assets must be a regulated qualified financial institution.

· Clear Definition as a Payment Medium: The bill explicitly defines stablecoin as a new type of payment medium, primarily regulated by the banking regulatory system, rather than restricted by the securities or commodities regulatory system.

· Embracing Existing Stablecoins: A maximum 18-month grace period after the bill's enactment, aimed at encouraging existing stablecoin issuers (such as USDT, USDC, etc.) to promptly obtain licenses or become compliant.

After finishing the main content, let's talk about the significance of this matter with an excited heart.

Over the years, when others asked, "After working in the Crypto industry for 16 years, what application have you created?"

In the future, you can confidently tell others—Stablecoins.

Some people have held opposing views. In the past, people's impression of stablecoins was that they were an opaque black box. Every few months, there would be FUD — whether Tether's assets were frozen or Circle had a significant black hole deficit.

In fact, if you think about it, Tether easily rakes in billions of dollars a year just from the interest on those underlying government bonds. Circle, slightly less, also made a $1.7 billion profit last year.

They basically made money while standing there. From a motivational standpoint, they have no malicious intentions. In fact, they are the most eager for compliance.

Now, this opaque black box will become a transparent white box.

In the past, the only complaint was that Tether's funds might have been frozen by the United States. Now, they will be directly placed into U.S. compliant custodial institutions, with high-frequency disclosures, so you can rest assured.

【No need to worry about a rug pull】 is such a huge advantage—I think especially all Crypto people understand this.

Stablecoins were once almost on the verge of being overtaken by CBDCs. In any country, if a central bank digital currency really exists, it is highly likely not built on a blockchain, at most it is built on some internal central bank consortium chain, which to be honest, is meaningless.

When CBDCs were at their peak, that was the most dangerous time for stablecoins.

If CBDCs had become a reality back then, stablecoins today would have been relentlessly suppressed into a dark corner, and blockchain would only be able to play a minimal role.

The remaining half-dead stablecoins would even have to learn the standards of central bank digital currencies, completely relinquishing their standard-setting power.

And now, stablecoins have won (or are about to).

Instead, everyone should learn the 【Blockchain + Token】 standard.

Nowadays, many blockchains actually have no meaningful applications on top, only stablecoin transfers. For example, with Aptos, the only scenario I use Aptos for is transfers between Binance and OKX.

And now, stablecoins will be legislated, what does that mean?

That's right, blockchain will become the only standard.

In the future, every stablecoin user will be the first to learn how to use a wallet.

As an aside, I actually think Ethereum's concerted push for EIP-7702 is quite forward-thinking. While other chains are all about memes, thank you Ethereum for sticking to account abstraction.

EIP-7702 is about Account Abstraction, which can support, for example:

· Social Account Registration Wallet

· Paying GAS with Native Coin

· And more

This paves the way for future new users to heavily use stablecoins, solving the last-mile problem.

Furthermore, once stablecoins receive legislative support, deposits and withdrawals will become even easier.

Let's imagine a scenario: previously, hindered by the gray nature of stablecoins, but after the bill passes, many traditional brokerages can support stablecoins themselves. The money from a US stock investor can be converted into stablecoins in minutes and instantly deposited into Coinbase. Believe it or not.

Let's imagine another scenario: if the brilliant bill smoothly passes through the House of Representatives, next, you will see:

Due to the extremely lucrative nature of this trading, existing stablecoin leaders and newly entering traditional giants will crazily start promoting their stablecoin products.

And an outsider, due to these promotions, will start using stablecoins. And then one day, after finding out that the wallet account has been created, will explore Bitcoin inside. Is mining Bitcoin difficult?

Stablecoins are a huge Trojan horse. The moment you start using stablecoins, you unwittingly step half a foot into the Crypto world.

As a large reservoir for digesting US debt, although stablecoins cannot directly absorb debt, they at least provide ammunition for the US debt secondary market. These functions are quite important, and slowly, stablecoins are becoming a part of the US debt market's body. Therefore, once the US legislation is passed and experiences the benefits, there is no turning back.

And, we are also confident that stablecoins are indeed one of the great innovations in our industry. People who have used stablecoins will find it hard to return to the traditional cash-banking system.

Once the bill is passed, users can't go back. In the future, concerns are about to be resolved, standards will be mastered, and the era of large deposits seems to be on the horizon.

Original Article Link

Pharos, deeply integrated with AntChain, is about to launch. How can we get involved?

$COIN Joins S&P 500, but Coinbase Isn't Celebrating

On May 13, S&P Dow Jones Indices announced that Coinbase would officially replace Discover Financial Services in the S&P 500 on May 19. While other companies like Block and MicroStrategy, closely tied to Bitcoin, were already part of the S&P 500, Coinbase became the first cryptocurrency exchange whose primary business is in the index. This also signifies that cryptocurrency is gradually moving from the fringes to the mainstream in the U.S.

On the day of the announcement, Coinbase's stock price surged by 23%, surpassing the $250 mark. However, just 3 days later, Coinbase was hit by two consecutive events: a hack where employees were bribed to steal customer data and a demand for a $20 million ransom, and an investigation by the U.S. Securities and Exchange Commission (SEC) into the authenticity of its claim of having over 100 million "verified users" in its securities filings and marketing materials. These two events acted as mini-bombs, and at the time of writing, Coinbase's stock had already dropped by over 7.3%.

Coincidentally, Discover Financial Services, being replaced by Coinbase, can also be considered the "Coinbase" of the previous payment era. Discover is a U.S.-based digital banking and payment services company headquartered in Illinois, founded in 1960. Its payment network, Discover Network, is the fourth largest payment network apart from Visa, Mastercard, and American Express.

In April, after the approval of the acquisition of Discover by the sixth-largest U.S. bank, Capital One, this well-established digital banking company of over 60 years smoothly handed over its S&P 500 "seat" to this emerging cryptocurrency "bank." This unexpected coincidence also portrayed the handover between the new and old eras in Coinbase's entry into the S&P 500, resembling a relay race scene. However, this relay baton also brought Coinbase's accumulated "external troubles and internal strife" to a tipping point.

Over the past decade, cryptocurrency exchanges have been the most stable "profit machines." They play a role in providing liquidity to the entire industry and rely on trading fees to sustain their operations. However, with the comprehensive rollout of ETF products in the U.S. market, this profit model is facing unprecedented challenges. As the leader in the "American stack," with over 80% of its business coming from the U.S., Coinbase is most affected by this.

Starting from the approval of Bitcoin and Ethereum spot ETFs, traditional financial capital has significantly onboarded users and funds that originally belonged to exchanges in a more cost-effective, compliant, and transparent manner. The transaction fee revenue of cryptocurrency exchanges has started to decline, and this trend may further intensify in the coming months.

According to Coinbase's 2024 Q4 financial report, the platform's total trading revenue was $417 million, a 45% year-on-year decrease. The contribution of BTC and ETH's trading revenue dropped from 65% in the same period last year to less than 50%.

This decline is not a result of a decrease in market enthusiasm. In fact, since the approval of the Bitcoin ETF in January 2024, the inflow of BTC into the U.S. market has continued to reach new highs, with asset management giants like BlackRock and Fidelity rapidly expanding their management scale. Data shows that BlackRock's iShares Bitcoin ETF (IBIT) alone has surpassed $17 billion in assets under management. As of mid-May 2025, the cumulative net inflow of 11 major institutional Bitcoin spot ETFs on the market has exceeded $41.5 billion, with a total net asset value of $1214.69 billion, accounting for approximately 5.91% of the total Bitcoin market capitalization.

Institutional investors and some retail investors are shifting towards ETF products, partly due to compliance and tax considerations. On one hand, ETFs have much lower trading costs compared to cryptocurrency exchanges. While Coinbase's spot trading fee rate varies annually in a tiered manner but averages around 1.49%, for example, the management fee for IBIT ETF is only 0.25%, and the majority of ETF institution fees fluctuate around 0.15% to 0.25%.

In other words, the more rational users are, the more likely they are to move from exchanges to ETF products, especially for investors aiming for long-term holdings.

According to multiple sources, several institutions, including VanEck and Grayscale, have submitted applications to the SEC for a Solana (SOL) ETF, with some institutions also planning to submit an XRP ETF proposal. Once approved, this may trigger a new round of fund migration. According to a report submitted by Coinbase to the SEC, as of April, the platform's trading revenue from XRP and Solana accounted for 18% and 10%, nearly one-third of the platform's fee revenue.

However, the Bitcoin and Ethereum ETFs passed in 2024 also reduced the fees for these two tokens on Coinbase from 30% and 15% to 26% and 10%, respectively. If the SOL and XRP ETFs are approved, it will further undermine the core fee revenue of exchanges like Coinbase.

The expansion of ETF products is gradually weakening the financial intermediary status of cryptocurrency exchanges. From their original roles as matchmakers and clearers to now gradually becoming mere "on-ramps and off-ramps" for funds, exchanges are seeing their marginal value squeezed by ETFs.

On May 12, 2025, SEC Chairman Paul S. Atkins gave a keynote speech at the Tokenization and Cryptocurrency Working Group roundtable. The theme of his speech revolved around "It is a new day at the SEC," where he indicated that the SEC would not approach enforcement and regulation the same way as before but would instead pave the way for cryptocurrency assets in the U.S. market.

With signs of cryptocurrency compliance such as the SEC's "NEW DAY" declaration, an increasing number of traditional brokerages are attempting to enter the cryptocurrency industry. One of the most representative cases is the well-known U.S. brokerage Robinhood, which began expanding its crypto business in 2018. By the time of its IPO in 2021, Robinhood's crypto business revenue accounted for over 50% of the company, with a significant boost from the Dogecoin "moonshot" promoted by Musk.

In Q1 2025 earnings report, Robinhood showcased strong growth, especially in revenue from cryptocurrency and options trading. Fueled by Trump's Memecoin, cryptocurrency-related revenue reached $250 million, nearly doubling year-over-year. Consequently, Robinhood Gold subscription users reached 3.5 million, a 90% increase from the previous year, with the rapid growth of Robinhood Gold providing the company with a stable source of income.

Meanwhile, RobinHood is actively pursuing acquisitions in the cryptocurrency space. In 2024, it announced a $2 billion acquisition of the long-standing European cryptocurrency exchange Bitstamp. Additionally, Canada's largest cryptocurrency CEX, WonderFi, which recently went public on the Toronto Stock Exchange, also announced its integration with RobinHood Crypto. After obtaining virtual asset licenses in the UK, Canada, Singapore, and other markets, RobinHood has taken a proactive approach in the compliant cryptocurrency trading market.

Furthermore, an increasing number of brokerage firms are exploring the same path. Futu Securities, Tiger Brokers, and others are also dipping their toes into cryptocurrency trading, with some having applied for or obtained the VA license from the Hong Kong SFC. Although their user bases are currently small, traditional brokerages have a natural advantage in user trust, regulatory licenses, and low fee structures. This could pose a threat to native cryptocurrency platforms in the future.

In April 2025, security researchers discovered that some Coinbase user data was leaked on the dark web. While the platform initially responded by attributing it to a "technical misinformation," it still raised concerns among users regarding its security and privacy protection. Just two days before Dow Jones Indexes announced Coinbase's addition to the S&P 500 Index, on May 11, 2025, Coinbase received an email from an unknown threat actor claiming to have obtained customer account information and internal documents, demanding a $20 million ransom to keep the data private. Subsequent investigations confirmed the data breach.

Cybercriminals obtained the data by bribing overseas customer service agents and support staff, mainly in "non-U.S. regions such as India." These agents abused their access to Coinbase's internal customer support system and stole customer data. As early as February this year, blockchain detective ZachXBT revealed on X platform that between December 2024 and January 2025, Coinbase users lost over $65 million to social engineering scams, with the actual amount potentially higher.

Among the victims was a well-known figure, 67-year-old Ed Suman, an established artist in the art world for nearly two decades, having been involved in the creation of artworks such as Jeff Koons' "Balloon Dog" sculpture. Earlier this year, he fell victim to an impersonation scam involving fake Coinbase customer support, resulting in a loss of over $2 million in cryptocurrency. ZachXBT critiqued Coinbase for its inadequate handling of such scams, noting that other major exchanges have not faced similar issues and recommending Coinbase to enhance its security measures.

Amidst a series of ongoing social engineering incidents, although there has not been any impact on user assets at the technical level so far, it has raised concerns among many retail and institutional investors. Especially institutions holding massive assets on Coinbase. Just considering the U.S. BTC ETF institutions, as of mid-May 2025, they collectively hold nearly 840,000 BTC, and 75% of these are custodied by Coinbase. If we price BTC at $100,000, this amount reaches a staggering $63 billion, which is equivalent to the nominal GDP of two Iceland in the year 2024.

In addition, Coinbase Custody also serves over 300 institutional clients, including hedge funds, family offices, pension funds, and endowments. As of the Q1 2025 financial report, Coinbase's total assets under management (including institutional and retail clients) reached $404 billion. The specific amount of institutional custodied assets was not explicitly disclosed in the latest report, but it should still be over 50% based on the Q4 2024 report.

Once this security barrier is breached, not only could the rate of user attrition far exceed expectations, but more importantly, institutional trust in it would undermine the foundation of its business. Therefore, after a hacking event, Coinbase's stock price plummeted significantly.

Facing a decline in spot trading fee revenue, Coinbase is also accelerating its transformation, attempting to find growth opportunities in derivatives and emerging assets. Coinbase acquired a stake in the options platform Deribit at the end of 2024 and announced the official launch of perpetual contract products in 2025. This acquisition fills in Coinbase's gap in options trading and its relatively small global market share.

Deribit has a strong presence in non-U.S. markets, especially in Asia and Europe. The acquisition has enabled Coinbase to gain a dominant position in bitcoin and ethereum options trading on Deribit, accounting for approximately 80% of the global options trading volume, with daily trading volume remaining above $2 billion.

Meanwhile, 80-90% of Deribit's customer base consists of institutional investors, with their professionalism and liquidity in the Bitcoin and Ethereum options market highly favored by institutions. Coinbase's compliance advantage, coupled with its already robust institutional ecosystem, makes it even more suitable. By using institutions as an entry point, it can face the squeeze from giants like Binance and OKX in the derivatives market.

Facing a similar dilemma is Kraken, which is attempting to replicate Binance Futures' model in non-U.S. markets. Since the derivatives market relies more on professional users, fee rates are relatively higher and stickiness is stronger, making it a significant source of revenue for exchanges. In the first half of 2025, Kraken completed the acquisition of TradeStation Crypto and a futures exchange, aiming to build a complete derivatives trading ecosystem to hedge the risk of declining spot transaction fee income.

With the surge of Memecoin in 2024, Binance, OKX, and various CEX platforms began massively listing small-market-cap, highly volatile tokens to activate active trading users. Due to the wealth effect and trading activity of Memecoins, Coinbase was also forced to join the battle, successively listing popular tokens from the Solana ecosystem such as BOOK OF MEME and Dogwifhat. Although these coins are controversial, they are frequently traded, with fee rates several times higher than mainstream coins, serving as a "blood-boosting" method for spot trading.

However, due to its status as a publicly traded company, this practice is a riskier endeavor for Coinbase. Even in the current crypto-friendly environment, the SEC is still investigating whether tokens like SOL, ADA, and SAND constitute securities.

In addition to the forced transformation strategies carried out by the aforementioned CEXs, they are also starting to lay out RWAs and the most talked-about stablecoin payment fields, such as the PYUSD launched through a collaboration between Coinbase and Paypal, Coinbase's support for the Euro stablecoin EURC by Circle that complies with EU MiCA regulatory requirements, or the USD1 launched through a collaboration between Binance and WIFL. In the increasingly crowded trading field, many CEXs have shifted their focus from just the trading market to the application field.

The golden age of transaction fees has quietly ended, and the second half of the crypto exchange platform game has silently begun.

Arthur Hayes: Why I'm Betting on ETH While the Market Is Obsessed with SOL

Key Market Insights for May 16th, how much did you miss out on?

CryptoPunks Changes Hands Twice, Did the Originator of NFTs Finally Find Its "Forever Home" This Time?

May 16 Key Market Information Gap, A Must-Read! | Alpha Morning Report

MOG Coin Skyrockets as Elon Musk and Garry Tan Embrace "mog/acc" Identity

The End and Rebirth of NFTs: How the Meme Coin Craze Ended the PFP Era?

STARTUP's Price Surges 40x in 30 Minutes: How did he become the Emotion King of Believe?

Key Market Intelligence on May 14th, how much did you miss out on?

1.Binance Alpha Launches HIPPO, BLUE, and Other Tokens

2.Believe Ecosystem Tokens See General Rise, LAUNCHCOIN Surges Over 250% in 24 Hours

3.Tiger Securities Introduces Cryptocurrency Deposit and Withdrawal Service, Supports Mainstream Cryptocurrencies such as BTC and ETH

4.Current Bitcoin Rally Possibly Driven by Institutions, Retail Traders Yet to Join

5.Binance Wallet's New TGE Privasea AI Participation Requires a 198 Point Threshold, with a Point Consumption of 15

Source: Overheard on CT (tg: @overheardonct), Kaito

PUMP: Today's discussions about PUMP focus on its new creator revenue-sharing model: the platform will allocate 50% of PumpSwap revenue to token creators, sparking varied reactions from users. Some criticize the move as insufficient or even misleading, while others view it as a positive step the platform is taking to reward creators. Meanwhile, PUMP faces market pressure from emerging competitors like LetsBONKfun and Raydium, which are rapidly gaining market share. Users also express concerns about PUMP's sustainability and potential regulatory risks in the U.S., with discussions extending to the platform's impact on the entire memecoin ecosystem.

COINBASE: Today, Coinbase became the first crypto company to join the S&P 500 Index, replacing Discover Financial Services, sparking widespread industry attention. The entire crypto community views this milestone as a significant development, signaling that crypto assets are further integrating into the mainstream financial system. The news has sparked lively discussions on Twitter, with many users pointing out that this may attract more institutional investors to enter the Bitcoin and other cryptocurrency markets.

XRP: XRP became the focal point of today's crypto discussion, with its significant market movements and strategic advances drawing attention. XRP has surpassed USDT to become the third-largest cryptocurrency by market capitalization, sparking market excitement and discussions about its future potential. The surge in market capitalization and price is believed to be related to increasing institutional interest, deepening strategic partnerships, and its role in the crypto ecosystem. Additionally, XRP's integration into multiple financial systems and its potential as a macro asset class are also seen as key factors driving the current market sentiment.

DYDX: Today's discussions about DYDX mainly focused on the dYdX Yapper Leaderboard launched by KaitoAI. The leaderboard aims to identify the most active community participants, with a total of $150,000 in rewards to be distributed over the first three seasons. This initiative has sparked broad community participation, with many users discussing the potential rewards and the incentive effect on the DYDX ecosystem. Meanwhile, progress on the ethDYDX to dYdX native chain migration and historical airdrop events have also been topics of discussion.

1. "What Is 'ICM'? Holding Up the $4 Billion Market Cap Solana's New Narrative"

Overnight, the hottest narrative in the crypto space has become "Internet Capital Markets," with a host of crypto projects and founders, led by the Solana ecosystem's new Launchpad platform Believe, releasing this phrase. Together with "Believe in something," it has become the new slogan heralding the onset of a bull market. What exactly is the so-called "Internet Capital Market," will it become a short-lived hype phrase like the Base ecosystem's previous Content Coin, and what related targets are available for selection?2.《LaunchCoin Surges 20x in One Day, How Did Believe Create a $200M Market Cap Shiba Inu After Going to Zero?|100x Retrospective》

LAUNCHCOIN broke through a $200 million market cap today, with the long-lost liquidity and such a high market cap "Memecoin" almost bringing half of the on-chain crypto community CT into the fray. The community is crazily discussing this token, with half of it being FOMO and the other half being FUD. This token, originally issued by Believe founder Ben Pasternak under his personal identity, transformed into a new platform token after a renaming. From once going to zero to a $200 million market cap, what happened in between?May 14 On-chain Fund Flow

Within 24 hours, GOONC's market cap soared to 70 million, could GOONC be the next billion-dollar dog on the Believe platform?

Bitcoin has broken $100,000, Ethereum has surpassed 2500, and is Solana's hot streak about to make a comeback?

The current market is in a state of macro euphoria, with GOONC riding the wave today, skyrocketing 10x in just a few hours, reaching a market cap of tens of millions of dollars, trading volume soaring past 50 million, and rumors swirling that the developer may be from OpenAI (unconfirmed but intriguing enough).

A ludicrous and absurd Solana meme that some actually buy into.

GOONC is a meme coin that has sprouted from the "gooning" subculture, offering no technological innovation or practical use, its sole function being speculation.

It takes inspiration from an NSFW term "gooning," which refers to a person being deeply immersed in certain content (you know what), eventually entering a nearly religious-like trance.

In Reddit (such as r/GOONED, r/GoonCaves) and some counterculture media outlets (such as MEL Magazine in 2020), "gooning" has gradually transitioned from an adult label to a meme-addicted, digital content and virtual self-indulgence synonym, arguably the epitome of Degen spirit.

GOONC is playing around with this concept, packaging the addictive nature, uselessness, and irony of gooning into a tradable financial product. The project team has made it clear: "We do not solve blockchain problems, we only trade absurdity." Blunt but oddly genuine.

GOONC launched on May 13, 2025, using the meme coin launch platform Believe App's LaunchCoin module on Solana. This tool is highly Degen: zero technical barriers, a few clicks to create a coin, perfect for projects like GOONC that can come up with ideas out of the blue.

The mastermind behind GOONC is also quite something and is the most talked-about, with KOL @basedalexandoor on X platform (alias "Pata van Goon") personally involved. His profile even caught the attention of Marc Andreessen, co-founder of a16z, making onlookers unable to resist speculating if GOONC has a hint of OpenAI lineage.

While this 'OpenAI Endorsement' is currently just community speculation, it is definitely a good card to play to fuel hype. Saying "we are pure speculation" on one hand, while tagging a few "AI + a16z" on the other.

GOONC took off as soon as it launched. After its launch on May 13, 2025, its market capitalization skyrocketed to $22 million within 4 hours, with a trading volume exceeding $25.6 million in 24 hours. According to platform data, the first day of trading saw an astonishing +41,100% surge, soaring from $0.0000001 to $0.02, becoming a "missed-the-boat" situation.

GOONC quickly formed an active trading community post-launch, with a lot of discussion and trading signals appearing on X platform (such as the 292x return signal provided by DeBot). Liquidity pools on exchanges like Raydium and Meteora grew rapidly, supporting high trading volumes and price increases.

The real climax occurred between May 13 and May 14, with the market cap rising to $5.5 million in the morning and directly surpassing $55 million in the afternoon. By the 14th, it briefly approached a $70 million market cap, with the trading volume soaring to $59 million. Some community members even posted screenshots claiming an increase of +85,000%, creating a new myth out of the ruins.

As of 1:30 pm on May 14, the price stabilized around $0.039, with a total market cap and FDV both around $39.6 million, and a 24-hour trading volume of $5.43 million. Active platforms include XT.COM, LBank, Meteora, and others.

Although there was a slight pullback from the peak ($0.07), the coin's popularity remains strong. For a coin that relies purely on "irony + community + X post" to thrive, this performance is already at a stellar level.

Currently, the background of the token's development team is not transparent, increasing the potential risk of a rug pull. Rugcheck.xyz warns that the creator of the GOONC contract may have permission to modify the contract (e.g., change fees or mint additional tokens), posing certain security risks.

Community members speculate that the meteoric rise of GOONC may be the "last hurrah".

After Surging 40%, Has Ethereum Price Peaked Upon Exiting the Craze?

Whether you are an insider or an outsider, these days you must be familiar with the news about Ethereum. The reason is simple, causing Ethereum enthusiasts to sigh with emotion and almost throwing off-guard those who defend Ethereum, Ethereum, with a "3-day surge of 40%," climbed to the top of the Douyin Hot List.

As we all know, Ethereum launched the Pectra upgrade on May 7th. This most significant network upgrade since early 2024 integrates the Prague execution layer hard fork and the Electra consensus layer upgrade, significantly improving Ethereum's performance through 11 improvement proposals. The account abstraction feature (EIP-7702) allows users to flexibly manage wallets through social media accounts or multi-signature schemes, reducing the user threshold, attracting more users and developers. The staking mechanism optimization increases the validator ETH cap from 32ETH to 2048ETH and introduces a flexible withdrawal method, making it easier for institutions and individuals to participate in network security, enhancing the market's confidence in Ethereum's long-term value.

At the same time, Pectra optimized the interaction efficiency of Layer 2 networks such as Arbitrum and Optimism, making transactions faster and cheaper, leading to a surge in on-chain activity. As a crucial step for Ethereum's transition from "2G" to "5G," the Pectra upgrade not only enhances network vitality but also "recharges confidence" in the market, directly driving the price increase.

Related Reading: "Ethereum Skyrockets 22% in One Day, E Enthusiasts Rejoice"

It's not just Ethereum itself, as Wall Street also brought important bullish news.

The world's largest asset management company, BlackRock, proposed to the SEC allowing Ethereum ETFs for staking. This proposal is expected to elevate Ethereum ETFs from a mere investment tool to a bond-like "interest-bearing asset," bringing investors both capital appreciation and passive income, igniting market optimism about Ethereum's future potential.

Specifically, BlackRock has proposed to amend its S-1 filing to allow investors to create and redeem ETF shares directly with Ethereum instead of the U.S. dollar (i.e., in-kind redemption). This move, combined with its $2.9 billion BUIDL Fund launched in March 2024, aims to deepen the integration of traditional finance with blockchain. The BUIDL Fund is a tokenized fund operating on the Ethereum network, investing in traditional assets such as U.S. Treasury bonds. This setup is highly attractive to institutional investors, as they can not only benefit from Ethereum's price appreciation but also earn stable cash flow through staking.

Robert Mitchnick, BlackRock's Head of Digital Assets, stated in a CNBC interview in March 2025 that the addition of staking functionality will significantly enhance the appeal of the Ethereum ETF. He admitted that when the Ethereum spot ETF was launched in July 2024 without staking functionality, the market demand was lackluster, and staking could be the key to reversing this trend.

Meanwhile, the SEC's shifting stance on cryptocurrency regulation has also fueled this upward trend. During the tenure of the previous SEC chairman, the regulatory approach was tough, and staking was strictly viewed through the Howey test as a potential unregistered security. Therefore, when approving the Ethereum spot ETF in May 2024, staking functionality was explicitly prohibited.

However, with Trump back in the White House and Paul Atkins taking over the SEC, there has been a noticeable relaxation in crypto regulation. Apart from BlackRock, ETF issuers such as Invesco Galaxy, VanEck, WisdomTree, and 21Shares have also submitted applications for similar staking and in-kind redemption.

Related reading: "New Chairman Takes Office, SEC Transforms into 'Crypto Daddy' Within 48 Hours"

If staking ETFs are approved, the benefits are likely to go beyond price appreciation. The introduction of staking functionality could redefine the role of crypto assets, making them more similar to traditional financial products that provide returns and value appreciation, thereby driving Ethereum closer to mainstream finance.

Currently, the SEC still needs to address several decisions related to crypto ETFs, including whether to approve ETFs for Solana, XRP, Litecoin, and even Dogecoin. With the calls for an "altcoin season" growing louder, Ethereum's strong performance may just be the beginning of a larger crypto market frenzy.

In addition, the Trump family-related DeFi project WLFI is also bullish on this wave of rise, with frequent on-chain activities. According to on-chain data analyst @ai_9684xtpa's monitoring, a WLFI-related address is currently borrowing coins to go long on ETH, borrowing 4 million U from Aave to buy 1590 ETH at an average price of $2515 per ETH.

For this epic surge of Ethereum after half a year of silence, the community has indeed gained more confidence and hope, which has also led to a revival of the entire altcoin market. However, amidst the joy, there are also voices of pessimism. Below is a summary conducted by BlockBeats based on community discussions.

The optimists point out that the current market structure is similar to the eve of the bull markets in 2016 and 2020, predicting a life-changing surge in the next 3-6 months, where some altcoins may even achieve astonishing single-day gains of up to 40%.

@liuwei16602825 stated that this surge signifies the return of the bull market as a sure thing. There is no need to worry about a pullback. The driving force behind the surge uses a high-cost isolated operation, fearing a drop more than any retail investor and will definitely do everything to support the price.

Related Reading: "Ethereum Leads the Surge Triggering the 'Altcoin Season' Speculation, How Do Traders View the Future Market?"

The bears mainly believe that this surge is different from the bull market of 2021, as the current market lacks the confidence of large-scale retail investors entering and holding positions for the long term, with funds rotating too quickly.

@market_beggar observed that a Bitfinex E/B whale has started to close positions and believes that if this whale maintains its high-speed position-closing operation for the next few days, it can be inferred that the whale no longer sees the upside potential of ETH, preparing to take profits and exit. The closing time will be a key focus going forward.

@FLS_OTC stated that there are still many uncertainties at the macro level, and the liquidity cannot support a major bull market. At this stage, it is a "last hurrah," not a complete reversal, and will continue to remain in a short position.

@off_thetarget believes that after ETH transitioned from POW to POS, it lost the "gold standard" of mining machine power cost support. The staking economic model led to a breakdown in value anchoring. Additionally, the L2 ecosystem (such as Starknet, zkSync, etc.) suffered from liquidity fragmentation, failing to establish an effective capital inflow mechanism, causing the collapse of the split disc pattern. Furthermore, the ETH community's excessive pursuit of technical narratives divorced from real-world needs resulted in a weak ecosystem growth. Therefore, he believes that ETH's intrinsic value system has crumbled, and the price is bound to plummet to the 800-1200 range, with a decisive short position at 1800.

@Airdrop_Guard, based on the core logic of the "High Probability Trading Strategy," where three sets of underlying logic different trading systems (such as volume depletion, price supply-demand, long/short position funding rate, etc.) simultaneously issue a short signal at the same point (2580), creating a high-probability trading opportunity. He emphasizes that these systems must be based on different algorithms and logics (rather than mere technical indicator overlays). The current ETH trend aligns with the short conditions in multiple independent dimensions of his trading system, hence the decision to short.

Overall, Bitcoin still maintains over 54% market dominance, and institutional funds' continued preference for it may limit the altcoin's upward potential. The market's future direction will depend on multiple factors, such as Bitcoin's price trend, global macroeconomic conditions, and whether funds can effectively rotate from Bitcoin to the altcoin sector.

Although Ethereum's recent leadership in the market has brought about optimistic sentiment, investors still need to remain rational as different sectors of altcoins are likely to show divergence in trends. Whether this round of Ethereum's rise will usher in a true altcoin frenzy may require more time and conducive conditions.

How to Get Rich in Crypto Without Relying on Luck? Financial Veteran Raoul Pal's Macro Insights and Investment Path

Stablecoins Driving Global B2B Payment Innovation: How to Break Through Workflow Bottlenecks and Unlock Trillion-Dollar Market Potential?

Which City Will Be the Crypto Capital? A Look at the 2025 Crypto-Friendly City Index

These startups are building cutting-edge AI models without the need for a data center

a16z Leads $18M Seed Round for Catena Labs, Crypto Industry Bets on Stablecoin AI Payment

Never Underestimate the Significance of the US Stablecoin 'Infrastructure Bill'

If the US stablecoin bill, the "GENIUS Act," passes smoothly this time, its significance will be tremendous. I even think it's significant enough to enter the top five in Crypto history.

Although abbreviated as the GENIUS Act, which translates directly to the Genius Act, it is actually the Guiding and Establishing National Innovation for U.S. Stablecoins, which translates to "Guiding and Establishing National Innovation for US Dollar Stablecoins."

The proposal is lengthy, with several key points summarized for everyone:

· Mandatory 1:1 Full Asset Backing: Assets include cash, demand deposits, and short-term US Treasuries. At the same time, misappropriation and rehypothecation are strictly prohibited.

· High-Frequency Disclosure: Reserve reports must be published at least monthly, introducing external audits.

· Licensing Requirement: Once the circulating market cap of the issuer's stablecoin exceeds $100 billion, it must transition into the federal regulatory system within a specified timeframe, adopting banking-grade regulation.

· Introduction of Custody: The custodian of the stablecoin and its reserve assets must be a regulated qualified financial institution.

· Clear Definition as a Payment Medium: The bill explicitly defines stablecoin as a new type of payment medium, primarily regulated by the banking regulatory system, rather than restricted by the securities or commodities regulatory system.

· Embracing Existing Stablecoins: A maximum 18-month grace period after the bill's enactment, aimed at encouraging existing stablecoin issuers (such as USDT, USDC, etc.) to promptly obtain licenses or become compliant.

After finishing the main content, let's talk about the significance of this matter with an excited heart.

Over the years, when others asked, "After working in the Crypto industry for 16 years, what application have you created?"

In the future, you can confidently tell others—Stablecoins.

Some people have held opposing views. In the past, people's impression of stablecoins was that they were an opaque black box. Every few months, there would be FUD — whether Tether's assets were frozen or Circle had a significant black hole deficit.

In fact, if you think about it, Tether easily rakes in billions of dollars a year just from the interest on those underlying government bonds. Circle, slightly less, also made a $1.7 billion profit last year.

They basically made money while standing there. From a motivational standpoint, they have no malicious intentions. In fact, they are the most eager for compliance.

Now, this opaque black box will become a transparent white box.

In the past, the only complaint was that Tether's funds might have been frozen by the United States. Now, they will be directly placed into U.S. compliant custodial institutions, with high-frequency disclosures, so you can rest assured.

【No need to worry about a rug pull】 is such a huge advantage—I think especially all Crypto people understand this.

Stablecoins were once almost on the verge of being overtaken by CBDCs. In any country, if a central bank digital currency really exists, it is highly likely not built on a blockchain, at most it is built on some internal central bank consortium chain, which to be honest, is meaningless.

When CBDCs were at their peak, that was the most dangerous time for stablecoins.

If CBDCs had become a reality back then, stablecoins today would have been relentlessly suppressed into a dark corner, and blockchain would only be able to play a minimal role.

The remaining half-dead stablecoins would even have to learn the standards of central bank digital currencies, completely relinquishing their standard-setting power.

And now, stablecoins have won (or are about to).

Instead, everyone should learn the 【Blockchain + Token】 standard.

Nowadays, many blockchains actually have no meaningful applications on top, only stablecoin transfers. For example, with Aptos, the only scenario I use Aptos for is transfers between Binance and OKX.

And now, stablecoins will be legislated, what does that mean?

That's right, blockchain will become the only standard.

In the future, every stablecoin user will be the first to learn how to use a wallet.

As an aside, I actually think Ethereum's concerted push for EIP-7702 is quite forward-thinking. While other chains are all about memes, thank you Ethereum for sticking to account abstraction.

EIP-7702 is about Account Abstraction, which can support, for example:

· Social Account Registration Wallet

· Paying GAS with Native Coin

· And more

This paves the way for future new users to heavily use stablecoins, solving the last-mile problem.

Furthermore, once stablecoins receive legislative support, deposits and withdrawals will become even easier.

Let's imagine a scenario: previously, hindered by the gray nature of stablecoins, but after the bill passes, many traditional brokerages can support stablecoins themselves. The money from a US stock investor can be converted into stablecoins in minutes and instantly deposited into Coinbase. Believe it or not.

Let's imagine another scenario: if the brilliant bill smoothly passes through the House of Representatives, next, you will see:

Due to the extremely lucrative nature of this trading, existing stablecoin leaders and newly entering traditional giants will crazily start promoting their stablecoin products.

And an outsider, due to these promotions, will start using stablecoins. And then one day, after finding out that the wallet account has been created, will explore Bitcoin inside. Is mining Bitcoin difficult?

Stablecoins are a huge Trojan horse. The moment you start using stablecoins, you unwittingly step half a foot into the Crypto world.

As a large reservoir for digesting US debt, although stablecoins cannot directly absorb debt, they at least provide ammunition for the US debt secondary market. These functions are quite important, and slowly, stablecoins are becoming a part of the US debt market's body. Therefore, once the US legislation is passed and experiences the benefits, there is no turning back.

And, we are also confident that stablecoins are indeed one of the great innovations in our industry. People who have used stablecoins will find it hard to return to the traditional cash-banking system.

Once the bill is passed, users can't go back. In the future, concerns are about to be resolved, standards will be mastered, and the era of large deposits seems to be on the horizon.

Original Article Link

Pharos, deeply integrated with AntChain, is about to launch. How can we get involved?

$COIN Joins S&P 500, but Coinbase Isn't Celebrating

On May 13, S&P Dow Jones Indices announced that Coinbase would officially replace Discover Financial Services in the S&P 500 on May 19. While other companies like Block and MicroStrategy, closely tied to Bitcoin, were already part of the S&P 500, Coinbase became the first cryptocurrency exchange whose primary business is in the index. This also signifies that cryptocurrency is gradually moving from the fringes to the mainstream in the U.S.

On the day of the announcement, Coinbase's stock price surged by 23%, surpassing the $250 mark. However, just 3 days later, Coinbase was hit by two consecutive events: a hack where employees were bribed to steal customer data and a demand for a $20 million ransom, and an investigation by the U.S. Securities and Exchange Commission (SEC) into the authenticity of its claim of having over 100 million "verified users" in its securities filings and marketing materials. These two events acted as mini-bombs, and at the time of writing, Coinbase's stock had already dropped by over 7.3%.

Coincidentally, Discover Financial Services, being replaced by Coinbase, can also be considered the "Coinbase" of the previous payment era. Discover is a U.S.-based digital banking and payment services company headquartered in Illinois, founded in 1960. Its payment network, Discover Network, is the fourth largest payment network apart from Visa, Mastercard, and American Express.

In April, after the approval of the acquisition of Discover by the sixth-largest U.S. bank, Capital One, this well-established digital banking company of over 60 years smoothly handed over its S&P 500 "seat" to this emerging cryptocurrency "bank." This unexpected coincidence also portrayed the handover between the new and old eras in Coinbase's entry into the S&P 500, resembling a relay race scene. However, this relay baton also brought Coinbase's accumulated "external troubles and internal strife" to a tipping point.

Over the past decade, cryptocurrency exchanges have been the most stable "profit machines." They play a role in providing liquidity to the entire industry and rely on trading fees to sustain their operations. However, with the comprehensive rollout of ETF products in the U.S. market, this profit model is facing unprecedented challenges. As the leader in the "American stack," with over 80% of its business coming from the U.S., Coinbase is most affected by this.

Starting from the approval of Bitcoin and Ethereum spot ETFs, traditional financial capital has significantly onboarded users and funds that originally belonged to exchanges in a more cost-effective, compliant, and transparent manner. The transaction fee revenue of cryptocurrency exchanges has started to decline, and this trend may further intensify in the coming months.

According to Coinbase's 2024 Q4 financial report, the platform's total trading revenue was $417 million, a 45% year-on-year decrease. The contribution of BTC and ETH's trading revenue dropped from 65% in the same period last year to less than 50%.

This decline is not a result of a decrease in market enthusiasm. In fact, since the approval of the Bitcoin ETF in January 2024, the inflow of BTC into the U.S. market has continued to reach new highs, with asset management giants like BlackRock and Fidelity rapidly expanding their management scale. Data shows that BlackRock's iShares Bitcoin ETF (IBIT) alone has surpassed $17 billion in assets under management. As of mid-May 2025, the cumulative net inflow of 11 major institutional Bitcoin spot ETFs on the market has exceeded $41.5 billion, with a total net asset value of $1214.69 billion, accounting for approximately 5.91% of the total Bitcoin market capitalization.

Institutional investors and some retail investors are shifting towards ETF products, partly due to compliance and tax considerations. On one hand, ETFs have much lower trading costs compared to cryptocurrency exchanges. While Coinbase's spot trading fee rate varies annually in a tiered manner but averages around 1.49%, for example, the management fee for IBIT ETF is only 0.25%, and the majority of ETF institution fees fluctuate around 0.15% to 0.25%.

In other words, the more rational users are, the more likely they are to move from exchanges to ETF products, especially for investors aiming for long-term holdings.

According to multiple sources, several institutions, including VanEck and Grayscale, have submitted applications to the SEC for a Solana (SOL) ETF, with some institutions also planning to submit an XRP ETF proposal. Once approved, this may trigger a new round of fund migration. According to a report submitted by Coinbase to the SEC, as of April, the platform's trading revenue from XRP and Solana accounted for 18% and 10%, nearly one-third of the platform's fee revenue.

However, the Bitcoin and Ethereum ETFs passed in 2024 also reduced the fees for these two tokens on Coinbase from 30% and 15% to 26% and 10%, respectively. If the SOL and XRP ETFs are approved, it will further undermine the core fee revenue of exchanges like Coinbase.

The expansion of ETF products is gradually weakening the financial intermediary status of cryptocurrency exchanges. From their original roles as matchmakers and clearers to now gradually becoming mere "on-ramps and off-ramps" for funds, exchanges are seeing their marginal value squeezed by ETFs.

On May 12, 2025, SEC Chairman Paul S. Atkins gave a keynote speech at the Tokenization and Cryptocurrency Working Group roundtable. The theme of his speech revolved around "It is a new day at the SEC," where he indicated that the SEC would not approach enforcement and regulation the same way as before but would instead pave the way for cryptocurrency assets in the U.S. market.

With signs of cryptocurrency compliance such as the SEC's "NEW DAY" declaration, an increasing number of traditional brokerages are attempting to enter the cryptocurrency industry. One of the most representative cases is the well-known U.S. brokerage Robinhood, which began expanding its crypto business in 2018. By the time of its IPO in 2021, Robinhood's crypto business revenue accounted for over 50% of the company, with a significant boost from the Dogecoin "moonshot" promoted by Musk.

In Q1 2025 earnings report, Robinhood showcased strong growth, especially in revenue from cryptocurrency and options trading. Fueled by Trump's Memecoin, cryptocurrency-related revenue reached $250 million, nearly doubling year-over-year. Consequently, Robinhood Gold subscription users reached 3.5 million, a 90% increase from the previous year, with the rapid growth of Robinhood Gold providing the company with a stable source of income.

Meanwhile, RobinHood is actively pursuing acquisitions in the cryptocurrency space. In 2024, it announced a $2 billion acquisition of the long-standing European cryptocurrency exchange Bitstamp. Additionally, Canada's largest cryptocurrency CEX, WonderFi, which recently went public on the Toronto Stock Exchange, also announced its integration with RobinHood Crypto. After obtaining virtual asset licenses in the UK, Canada, Singapore, and other markets, RobinHood has taken a proactive approach in the compliant cryptocurrency trading market.

Furthermore, an increasing number of brokerage firms are exploring the same path. Futu Securities, Tiger Brokers, and others are also dipping their toes into cryptocurrency trading, with some having applied for or obtained the VA license from the Hong Kong SFC. Although their user bases are currently small, traditional brokerages have a natural advantage in user trust, regulatory licenses, and low fee structures. This could pose a threat to native cryptocurrency platforms in the future.

In April 2025, security researchers discovered that some Coinbase user data was leaked on the dark web. While the platform initially responded by attributing it to a "technical misinformation," it still raised concerns among users regarding its security and privacy protection. Just two days before Dow Jones Indexes announced Coinbase's addition to the S&P 500 Index, on May 11, 2025, Coinbase received an email from an unknown threat actor claiming to have obtained customer account information and internal documents, demanding a $20 million ransom to keep the data private. Subsequent investigations confirmed the data breach.

Cybercriminals obtained the data by bribing overseas customer service agents and support staff, mainly in "non-U.S. regions such as India." These agents abused their access to Coinbase's internal customer support system and stole customer data. As early as February this year, blockchain detective ZachXBT revealed on X platform that between December 2024 and January 2025, Coinbase users lost over $65 million to social engineering scams, with the actual amount potentially higher.

Among the victims was a well-known figure, 67-year-old Ed Suman, an established artist in the art world for nearly two decades, having been involved in the creation of artworks such as Jeff Koons' "Balloon Dog" sculpture. Earlier this year, he fell victim to an impersonation scam involving fake Coinbase customer support, resulting in a loss of over $2 million in cryptocurrency. ZachXBT critiqued Coinbase for its inadequate handling of such scams, noting that other major exchanges have not faced similar issues and recommending Coinbase to enhance its security measures.

Amidst a series of ongoing social engineering incidents, although there has not been any impact on user assets at the technical level so far, it has raised concerns among many retail and institutional investors. Especially institutions holding massive assets on Coinbase. Just considering the U.S. BTC ETF institutions, as of mid-May 2025, they collectively hold nearly 840,000 BTC, and 75% of these are custodied by Coinbase. If we price BTC at $100,000, this amount reaches a staggering $63 billion, which is equivalent to the nominal GDP of two Iceland in the year 2024.

In addition, Coinbase Custody also serves over 300 institutional clients, including hedge funds, family offices, pension funds, and endowments. As of the Q1 2025 financial report, Coinbase's total assets under management (including institutional and retail clients) reached $404 billion. The specific amount of institutional custodied assets was not explicitly disclosed in the latest report, but it should still be over 50% based on the Q4 2024 report.

Once this security barrier is breached, not only could the rate of user attrition far exceed expectations, but more importantly, institutional trust in it would undermine the foundation of its business. Therefore, after a hacking event, Coinbase's stock price plummeted significantly.

Facing a decline in spot trading fee revenue, Coinbase is also accelerating its transformation, attempting to find growth opportunities in derivatives and emerging assets. Coinbase acquired a stake in the options platform Deribit at the end of 2024 and announced the official launch of perpetual contract products in 2025. This acquisition fills in Coinbase's gap in options trading and its relatively small global market share.

Deribit has a strong presence in non-U.S. markets, especially in Asia and Europe. The acquisition has enabled Coinbase to gain a dominant position in bitcoin and ethereum options trading on Deribit, accounting for approximately 80% of the global options trading volume, with daily trading volume remaining above $2 billion.

Meanwhile, 80-90% of Deribit's customer base consists of institutional investors, with their professionalism and liquidity in the Bitcoin and Ethereum options market highly favored by institutions. Coinbase's compliance advantage, coupled with its already robust institutional ecosystem, makes it even more suitable. By using institutions as an entry point, it can face the squeeze from giants like Binance and OKX in the derivatives market.

Facing a similar dilemma is Kraken, which is attempting to replicate Binance Futures' model in non-U.S. markets. Since the derivatives market relies more on professional users, fee rates are relatively higher and stickiness is stronger, making it a significant source of revenue for exchanges. In the first half of 2025, Kraken completed the acquisition of TradeStation Crypto and a futures exchange, aiming to build a complete derivatives trading ecosystem to hedge the risk of declining spot transaction fee income.

With the surge of Memecoin in 2024, Binance, OKX, and various CEX platforms began massively listing small-market-cap, highly volatile tokens to activate active trading users. Due to the wealth effect and trading activity of Memecoins, Coinbase was also forced to join the battle, successively listing popular tokens from the Solana ecosystem such as BOOK OF MEME and Dogwifhat. Although these coins are controversial, they are frequently traded, with fee rates several times higher than mainstream coins, serving as a "blood-boosting" method for spot trading.

However, due to its status as a publicly traded company, this practice is a riskier endeavor for Coinbase. Even in the current crypto-friendly environment, the SEC is still investigating whether tokens like SOL, ADA, and SAND constitute securities.

In addition to the forced transformation strategies carried out by the aforementioned CEXs, they are also starting to lay out RWAs and the most talked-about stablecoin payment fields, such as the PYUSD launched through a collaboration between Coinbase and Paypal, Coinbase's support for the Euro stablecoin EURC by Circle that complies with EU MiCA regulatory requirements, or the USD1 launched through a collaboration between Binance and WIFL. In the increasingly crowded trading field, many CEXs have shifted their focus from just the trading market to the application field.

The golden age of transaction fees has quietly ended, and the second half of the crypto exchange platform game has silently begun.

Arthur Hayes: Why I'm Betting on ETH While the Market Is Obsessed with SOL

Key Market Insights for May 16th, how much did you miss out on?

Popular coins

Latest Crypto News

Customer Support:@weikecs

Business Cooperation:@weikecs

Quant Trading & MM:bd@weex.com

VIP Services:support@weex.com